This article provides an analytical overview of the pharmaceutical retail market for 9 months of 2024, key trends and forecasts for 2025. It is based on the report presented at the Pharmexpert 2024 Forum by Tatiana Ivanova, Product Manager of Proxima Research’s Ukrainian Market Audit product.

Retail and hospital drug consumption

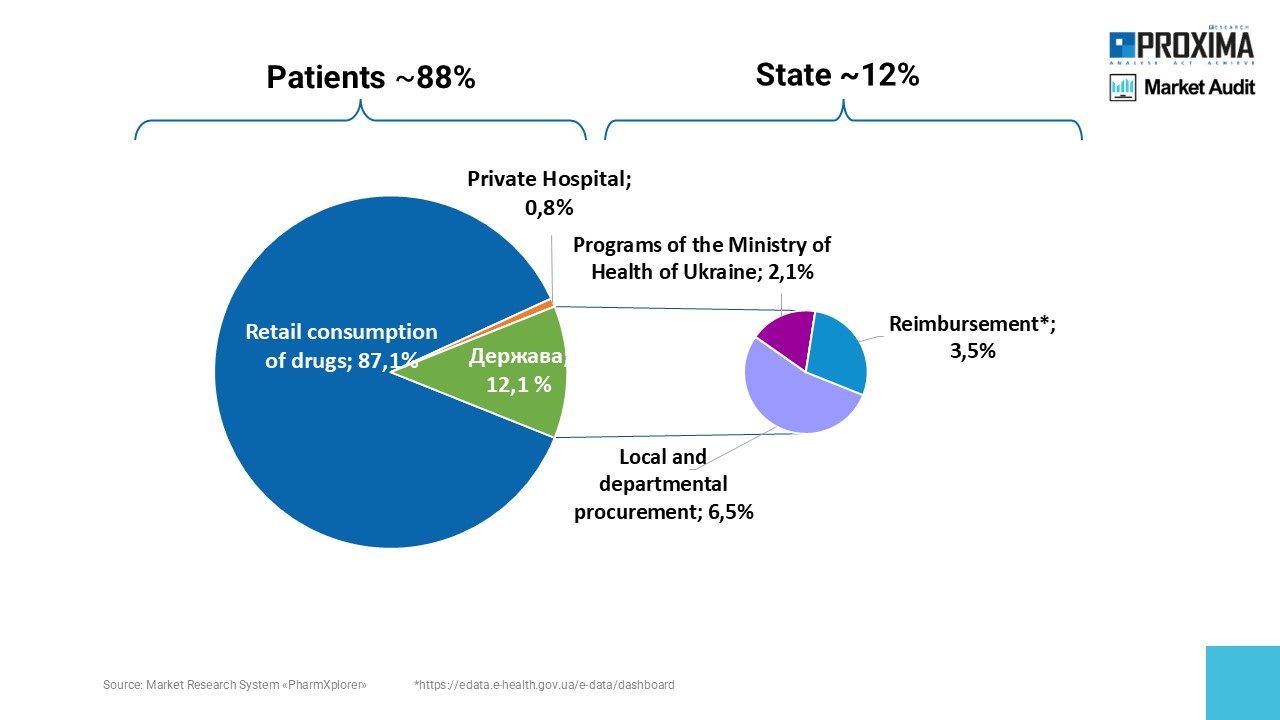

The retail segment accounts for the vast majority of total drug consumption in Ukraine (Fig. 1). According to the results of 9 months of 2024, the state covers 12% of consumption with its programs, and 88% is consumed by patients at their own expense. Thus, the development of the Ukrainian pharmaceutical market depends almost entirely on the welfare of the consumer.

Fig. 1. Structure of drugs consumption by sources of financing

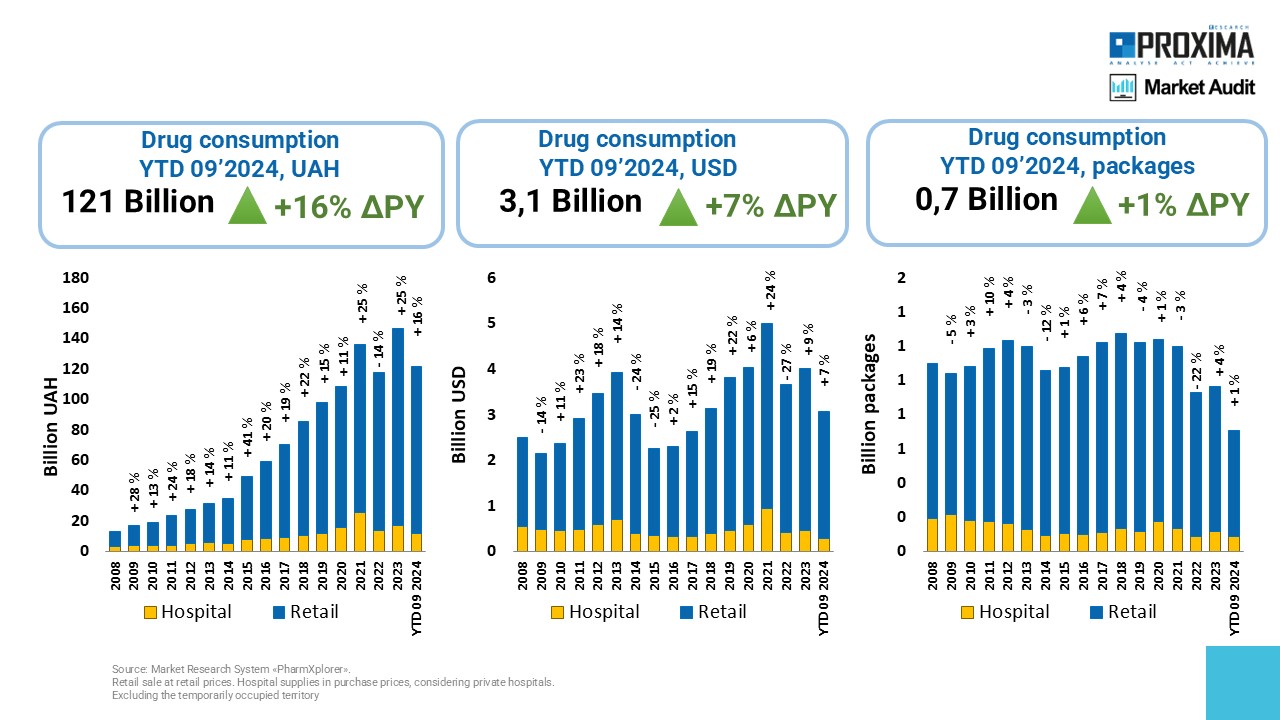

The pharmaceutical market was expected to show positive dynamics in 2024. In the first 9 months of the year, retail and hospital consumption increased by 16% in national currency and by 7% in dollar terms compared to the same period of the previous year (Fig. 2). In physical terms, there was an increase of 1%.

Fig. 2. Dynamics of retail drug sales in terms of hospital and retail consumption from 2008 to 9 months of 2024

Retail drug sales

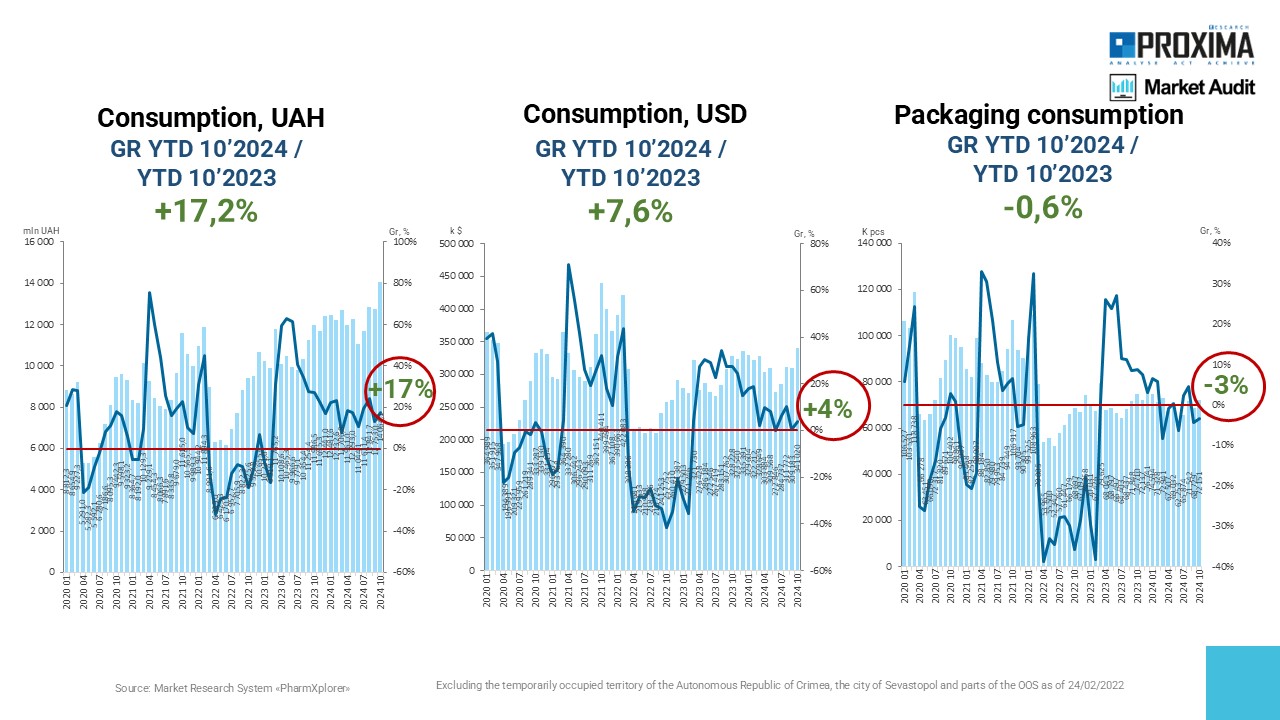

Retail drug consumption in the first 10 months of 2024 also showed strong growth of 17.2% in hryvnia (Fig. 3). In dollar terms, the increase was 7.6%. In physical terms, the market remains almost at the same level as in the same period of previous year. This is caused, among other things, to the fact that part of the population went abroad due to the outbreak of a full-scale war, so unfortunately, we are currently experiencing a decrease in the number of available population.

Fig. 3. Monthly dynamics of retail drug sales in monetary, physical and dollar terms from January 2020 to October

The main driver of the market growth is the inflationary component, as well as the redistribution of consumption towards more expensive drugs and larger packages.

The structure of consumption in terms of domestic and foreign manufacturers has stabilized in the following ratio. In monetary terms, foreign players account for 63% of retail sales of drugs and domestic players for 37%. In physical terms, on the contrary, 62% are domestic drugs, and 38% are foreign drugs.

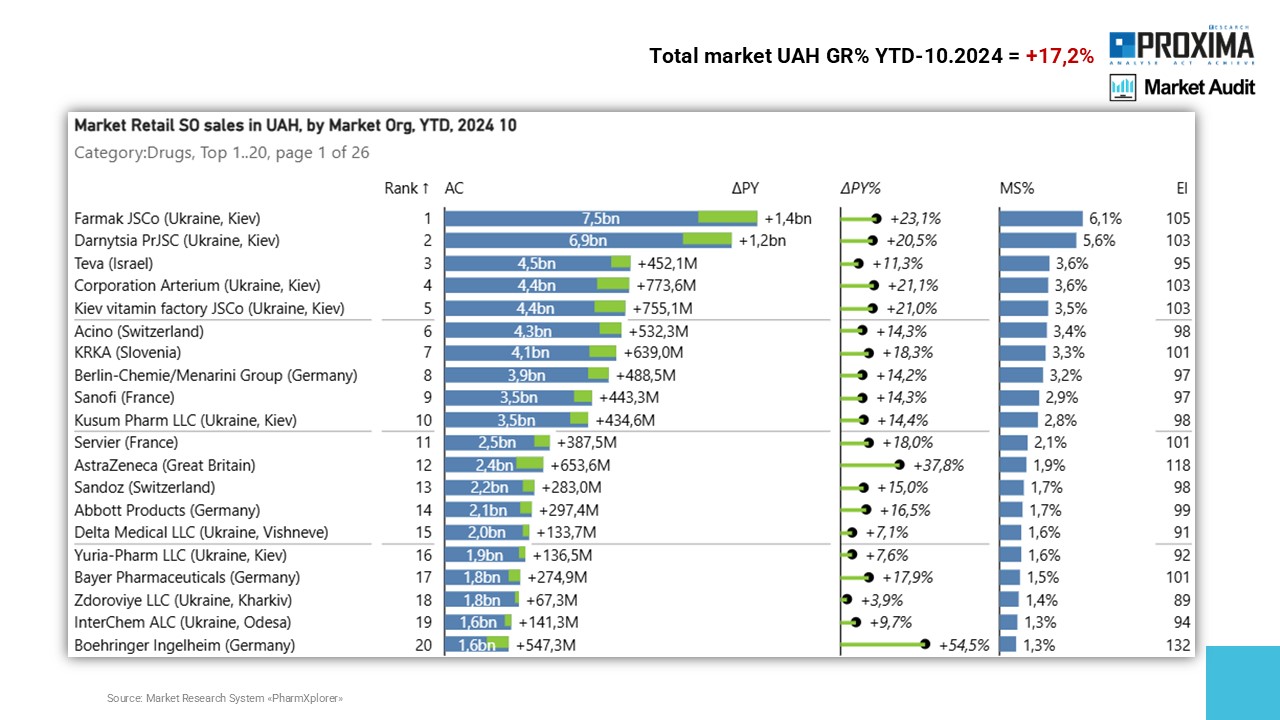

The ranking of marketing organizations in terms of pharmacy drug sales in 10 months of 2024 is headed by domestic pharmaceutical companies Farmak and Darnitsa (Fig. 4). Teva, Arterium Corporation and Kyiv Vitamin Plant round out the top five. Thus, four of the top 5 companies are Ukrainian. Among the top 20 marketing organizations, all companies demonstrate active growth in monetary terms.

Fig. 4. Top 20 marketing companies in terms of retail sales of medicinal products in 10 months of 2024

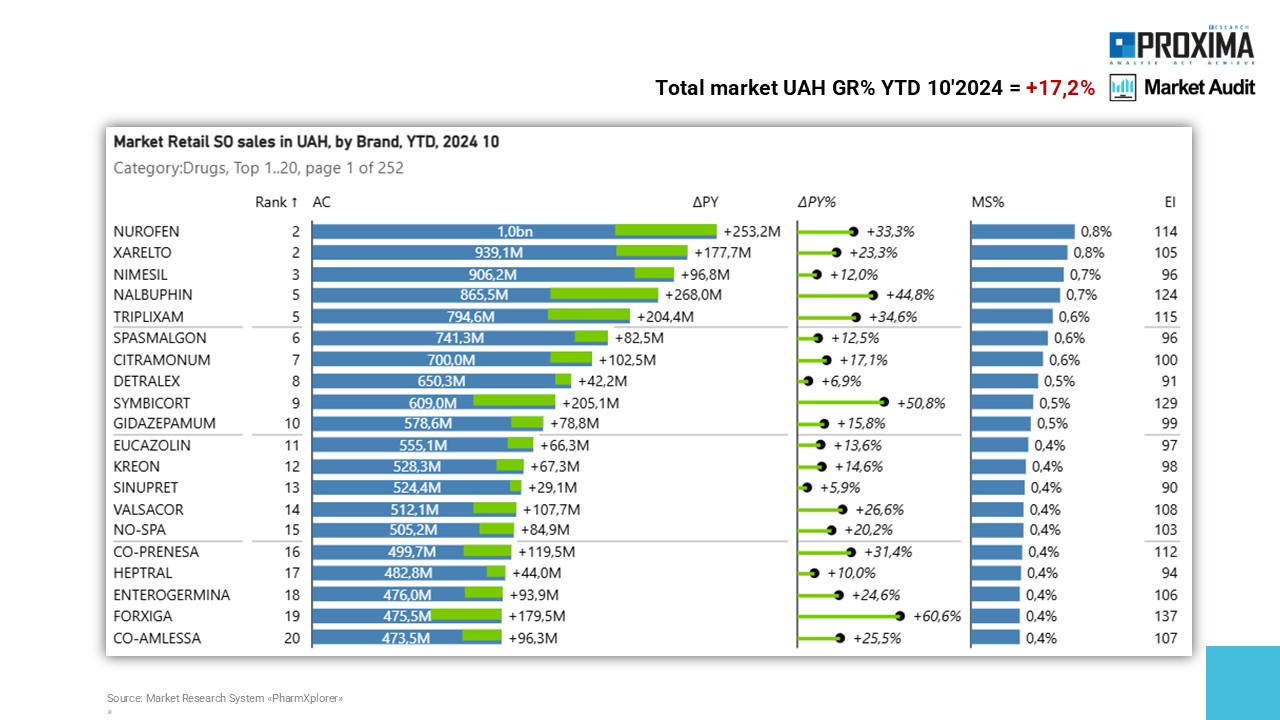

Nurofen, Xarelto, and Nimesil lead the ranking of drug brands in terms of pharmacy sales (Fig. 5).

Fig. 5. Top 20 drug brands by retail sales in 10 months of 2024

Trends in “pharmacy basket” structure

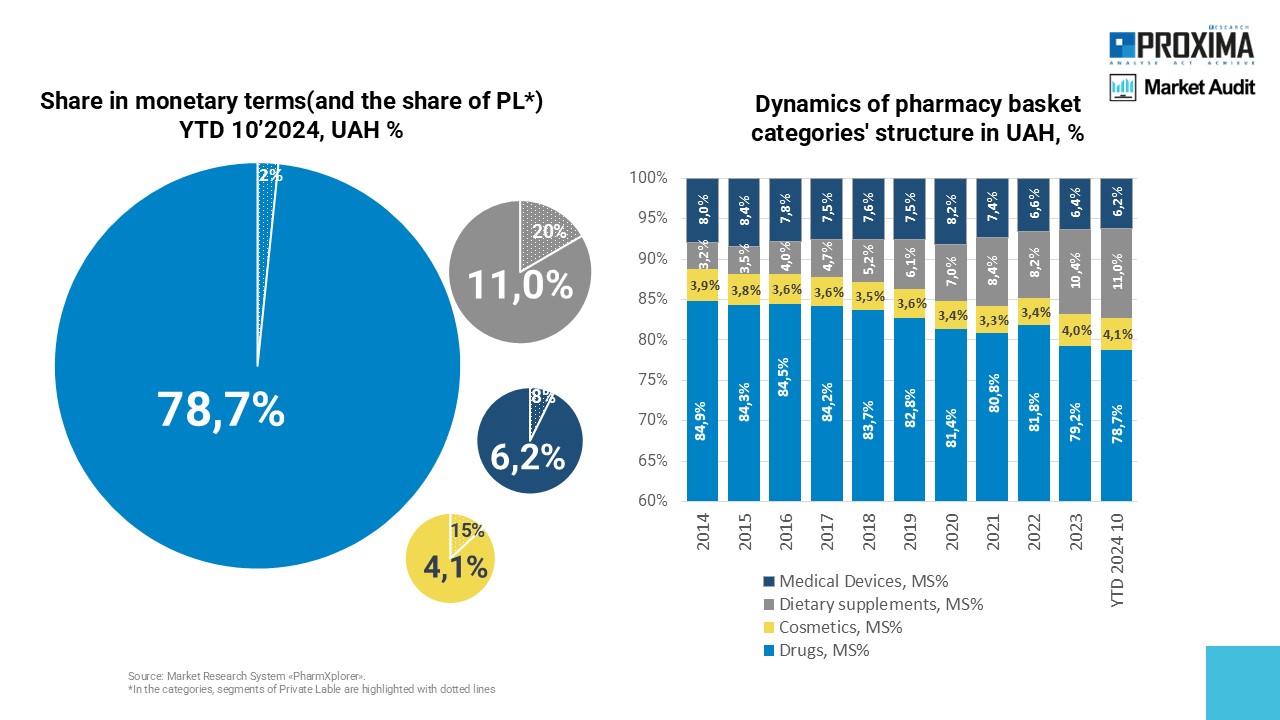

A long-term trend is an active increase in the share of dietary supplements in the structure of pharmacy sales of “pharmacy basket” goods (which includes drugs, medical devices, dietary supplements and cosmetics). According to the results of 10 months of 2024, their share reached 11% (Fig. 6). This category also has the highest representation of pharmacy chains’ own brands (OBCs) at 20%.

Fig. 6. Dynamics of different categories of goods share in the “pharmacy basket” from 2024 to 10 months 2024 in monetary terms, indicating the share of private label products in each category based on the results of 10 months of 2024.

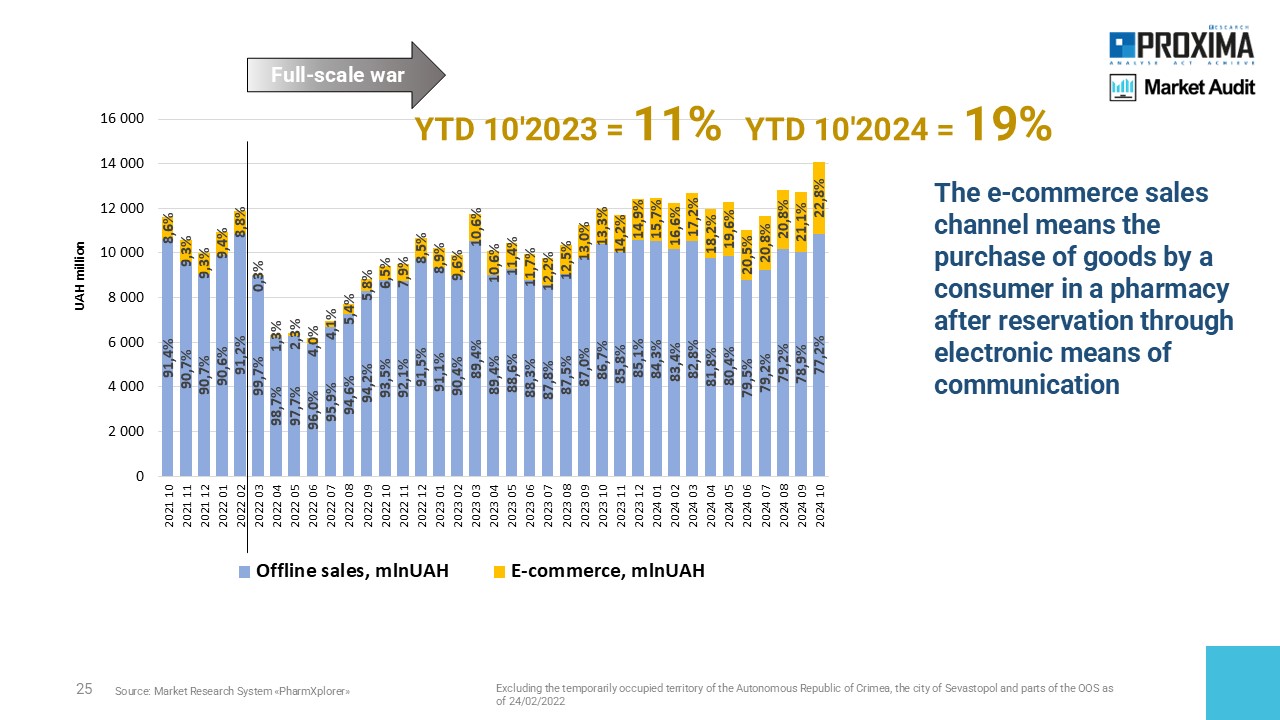

E-commerce

The e-commerce segment is showing dynamic development with double-digit growth rates. It means the redemption of goods by the consumer in a pharmacy after reservation through electronic means of communication. According to the results of 10 months of 2024, its share increased to 19% compared to 11% in the same period of 2023 (Fig. 7).

Fig. 7. Monthly dynamics of drug sales in terms of offline sales and e-commerce from October 2021 to October 2024

Farmak is the leader in e-commerce sales. The top 5 also includes Acino, Darnitsa, Kyiv Vitamin Plant, and KRKA. Other brands include Xarelto, Detralex, Triplixam, Heptral, and Nurofen. As a rule, the more expensive a drug is and the lower its market penetration, the higher its share in e-commerce will be, as consumers are looking for where to buy the drug at the best price online.

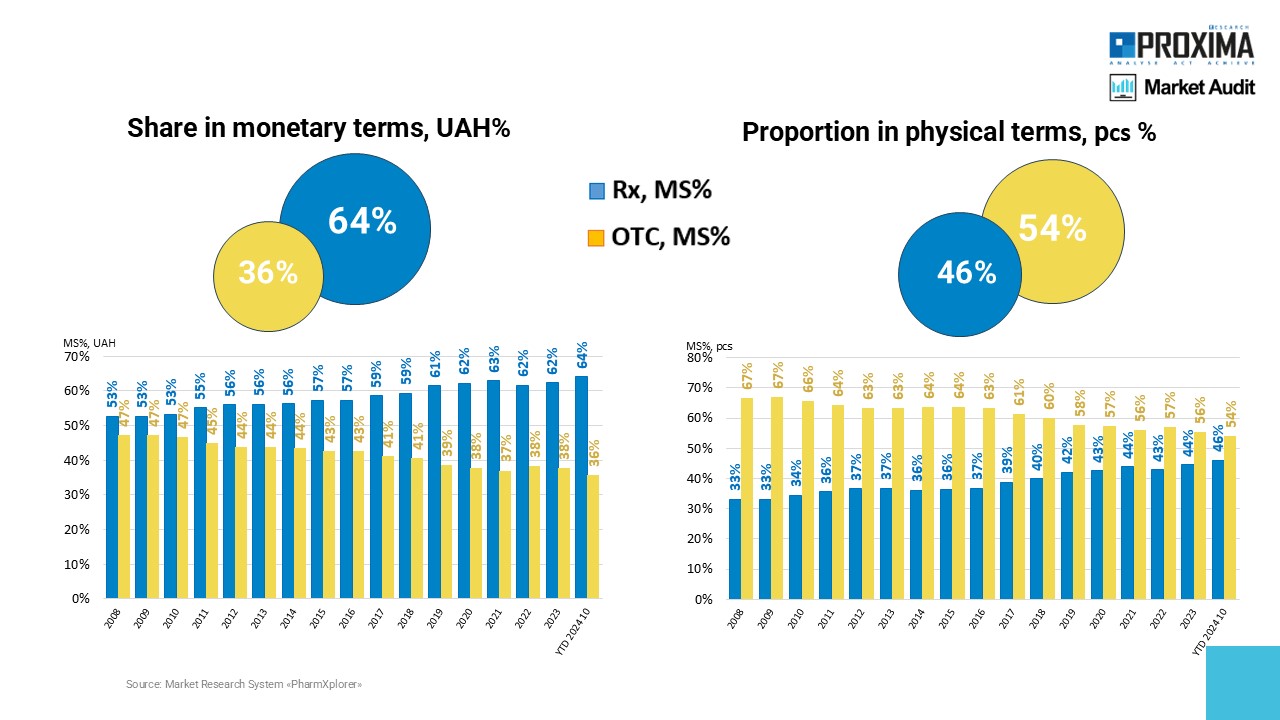

Rx VS OTC

The share of drugs prescription in total sales is steadily growing both in monetary and physical terms (Fig. 8). This trend has been observed for quite some time. According to the results of 10 months of 2024, the share of Rx drugs in monetary terms is 64% and 46% in packages.

Fig. 8. Dynamics of drugs retail sales by prescription status from 2008 to 9 months of 2024

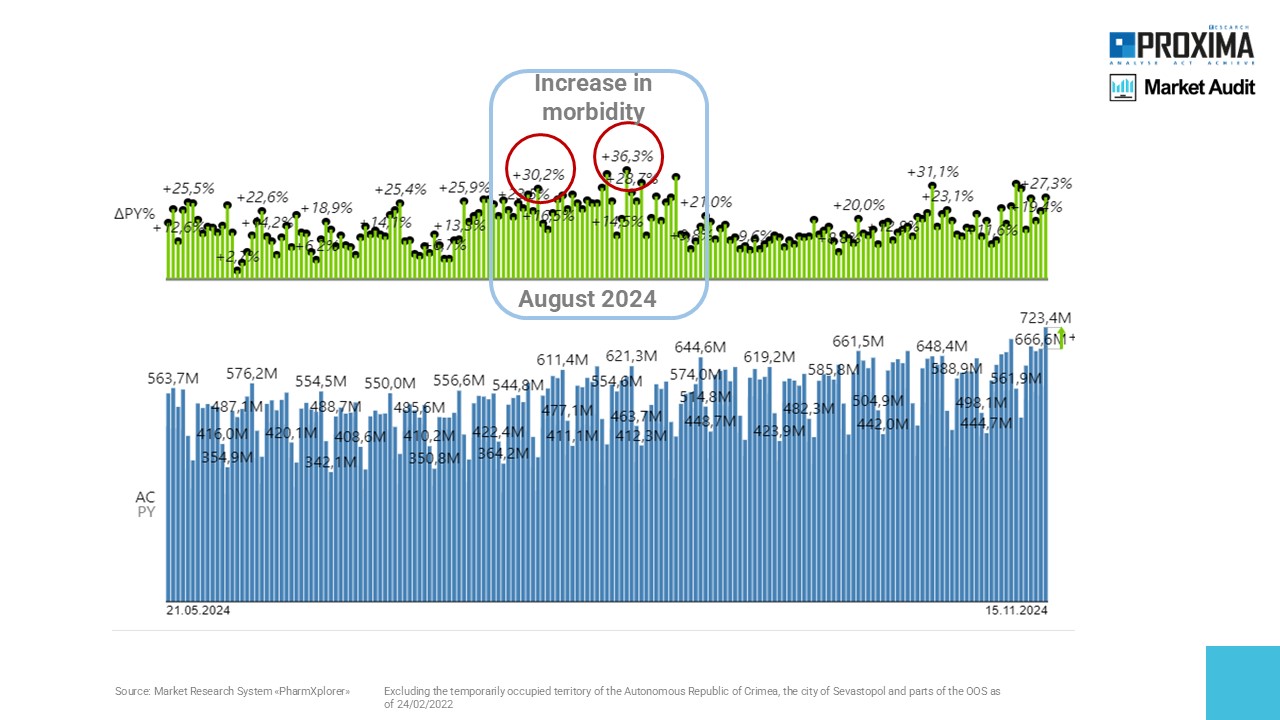

Seasonal trends

This year, a surge in the incidence of SARS occurred unexpectedly in August (Figure 9). In order not to miss such abnormal surges, which lead to an increase in demand for the relevant drugs, it is advisable to monitor the market dynamics daily.

Fig. 9. Daily dynamics of drug retail sales

In terms of drug classes, this period saw an increase in sales of drugs used for throat diseases and analgesics, which are often prescribed for SARS.

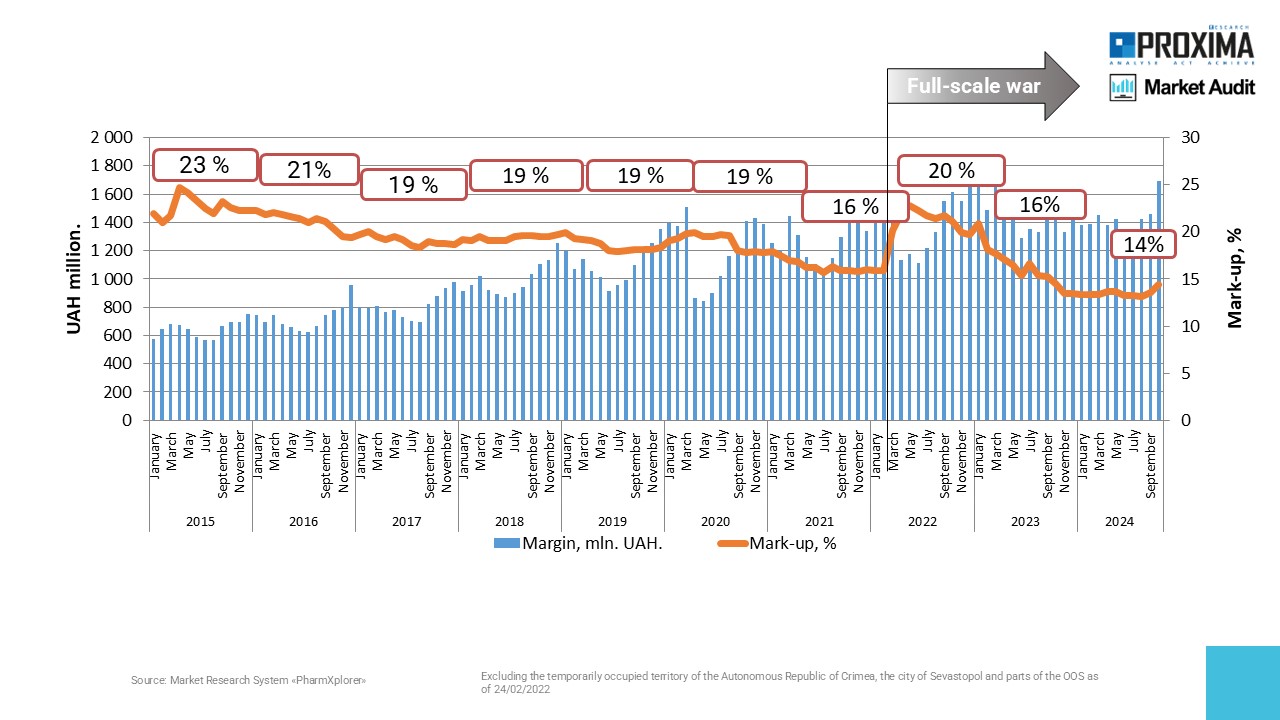

Price segments and margins

Let’s look at the structure of retail drug consumption in terms of price segments. The largest segment in monetary terms is drugs costing between UAH 125 and UAH 600. Its share is 60%. In physical terms, 53% of sales are accounted for by products costing up to UAH 125 and 42% by drugs costing between UAH 125 and UAH 600.

In the price segment up to UAH 125, Citramon, Captopress, Sodium chloride, Pancreatin, and Paracetamol are the leaders in terms of sales in monetary terms. Among the drugs priced at UAH 125-600, Nimesil, Nurofen, Triplixam, Nalbuphine and Detralex have the highest sales volumes. In the segment of UAH 600-1150, the leaders are Symbicort, Xarelto, Forksiga, Pulmicort and Fanigan. In the most expensive segment (over UAH 1,150), the best-selling drugs are Heptral, Sinjardi, Xarelto and Kitruda.

The weighted average pharmacy margin shows a long-term downward trend. Only at the beginning of 2022, due to the outbreak of a full-scale war, this figure increased sharply to 20%, but soon declined again. Currently, the weighted average pharmacy margin is below the pre-war level and amounts to 14% (Fig. 10).

Fig. 10. Monthly dynamics of changes in the weighted average pharmacy margin from January 2015 to October 2024

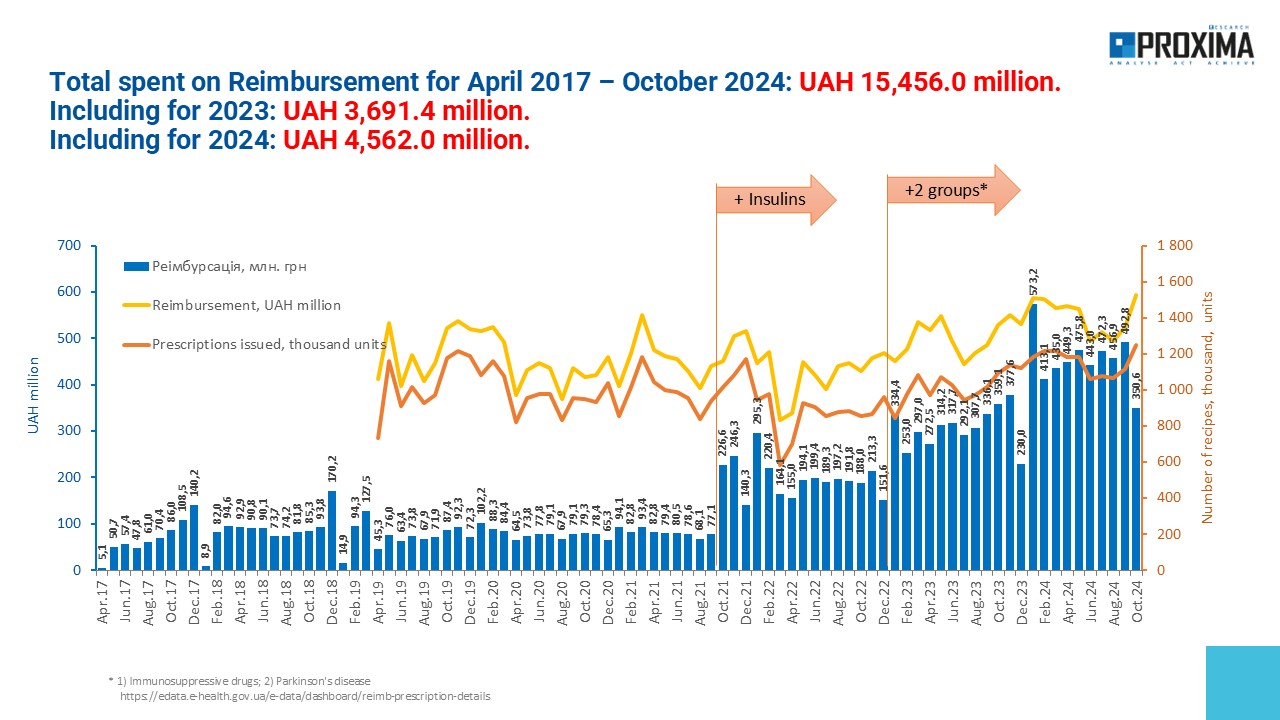

Reimbursement

Since the beginning of the state reimbursement program, the state had spent UAH 14.4 billion on drug reimbursement from April 2017 to October 2024. Of this amount, UAH 4.5 billion was spent in 2024 (Fig. 11). Over the years, the list of drugs subject to reimbursement had been expanding. Nevertheless, in the overall reimbursement market, reimbursed drugs had a rather small share (at 2%).

Fig. 11. Monthly dynamics of reimbursement of pharmacies for drugs under the “Affordable Drugs” program from April 2017 to October 2024

In addition, if we compare the prices listed in the Register of Drugs Eligible for Reimbursement under the Affordable Medicines Program and the weighted average prices in the retail segment by INN, we can see that in many cases the reference price (as specified in the MOH reimbursement orders) is higher than the weighted average retail price.

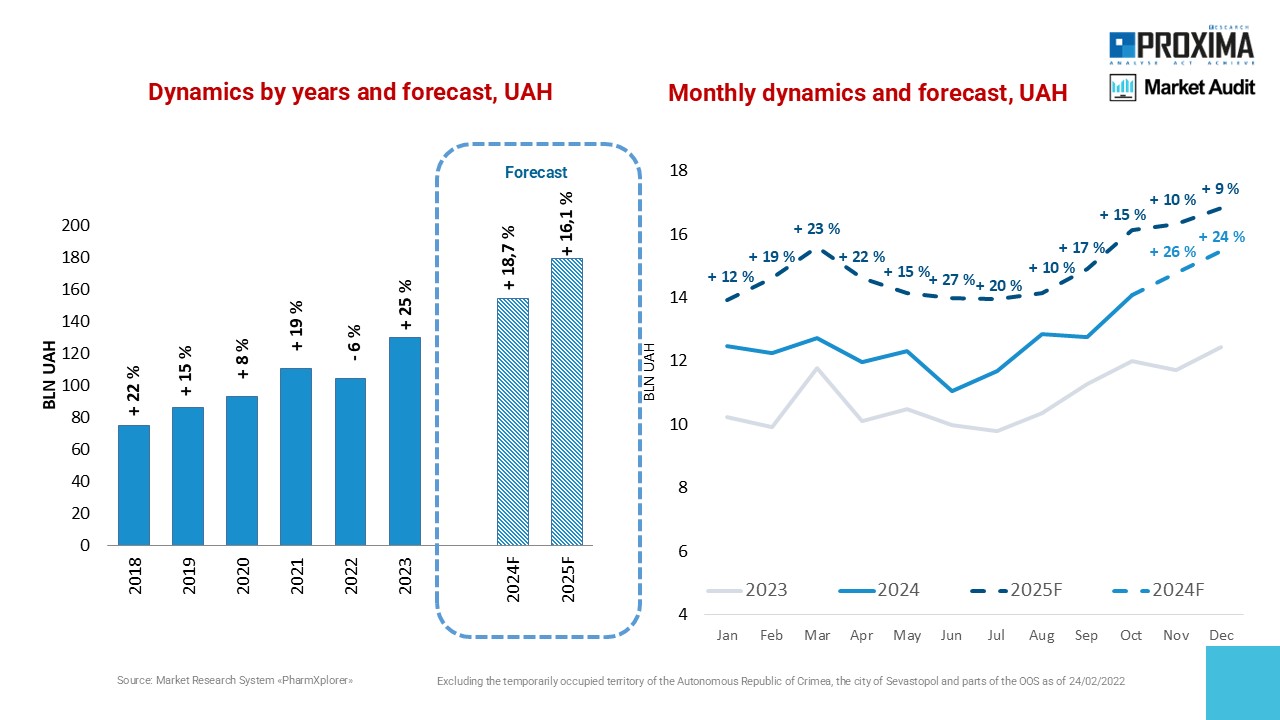

Forecasts for the development of the pharmaceutical retail market in 2025

By the end of 2024 year, the growth of the pharmacy drug market may reach 18.7% in hryvnia terms (Fig. 12). In 2025, the growth trend is expected to continue in national currency. The growth rate is expected to reach 16% under the baseline scenario. The data on the chart is displayed in two ways: the dense line represents the results already recorded, and the dashed line represents the forecast data.

Fig. 12. Forecast of the development of the retail drug sales market in 2024-2025 in national currency, as of the end of October 2024.

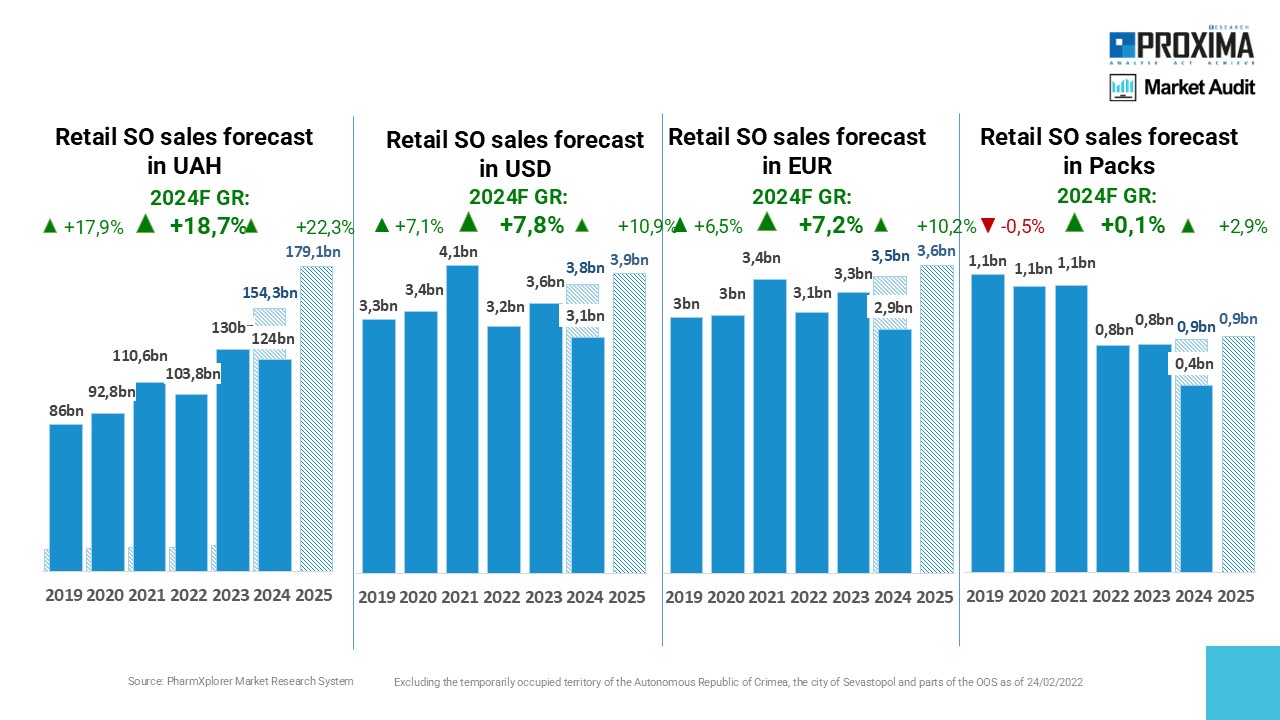

As for the forecasts in terms of other dimensions, the pharmaceutical market may grow by 7.8% in US dollars by 2024, by 7.2% in euros, and by 0.1% in packages (Fig. 13). This data is already available to users who have switched to the updated Power BI platform.

Fig. 13. Forecast for the development of the pharmaceutical retail market in 2024-2025 in USD, EUR and packs, as of the end of October 2024.

Results

Pharmaceutical sales continue to show positive dynamics after a significant decline caused by the full-scale war. As the retail segment accounts for the majority of total spending on drugs, the further development of the pharmaceutical market is highly dependent on consumer welfare.

The main factors driving growth are rising prices and a redistribution of consumption towards more expensive drugs. Opportunities for growth in packaged goods are very limited due to the fact that most of the population has gone abroad due to the full-scale war.

The share of dietary supplements is increasing significantly in the pharmacy basket category. This category also has the largest share of FMCG.

The e-commerce segment continues to grow rapidly. The larger the share of a drug on the market in general, the greater the share of e-commerce in it.

As for the market development forecast for 2025, the market for retail sales of drugs in hryvnia terms is expected to grow by 16.1% under the baseline scenario.

Learn more about the capabilities of the Market Audit product from Proxima Research. Order a presentation.

Order