Europe

As a result of the Russian Federation’s military aggression against Ukraine, the population is forced to make strategic reserves of water, food, and medicine, etc., especially for people with chronic illnesses. Lines to pharmacies began to form from the first minutes of the Russian invasion. The greater demand contributed to a significant increase in the volume of pharmacy drug sales. At the same time, not all pharmacies are operating now, find the most current data on the work of pharmacies on the map here. In addition, the opening hours of pharmacies in regions with a high probability of hostilities, bombing, and shelling have been significantly reduced. Data from the analytical system of market research «PharmXplorer» by Proxima Research International were used while preparing this material.

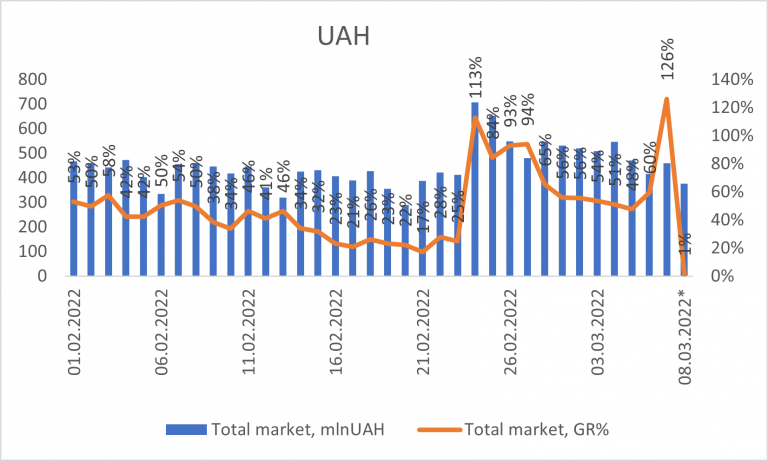

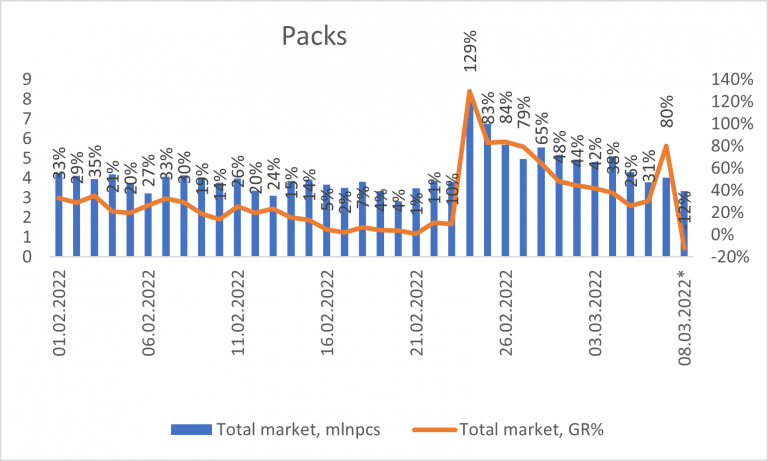

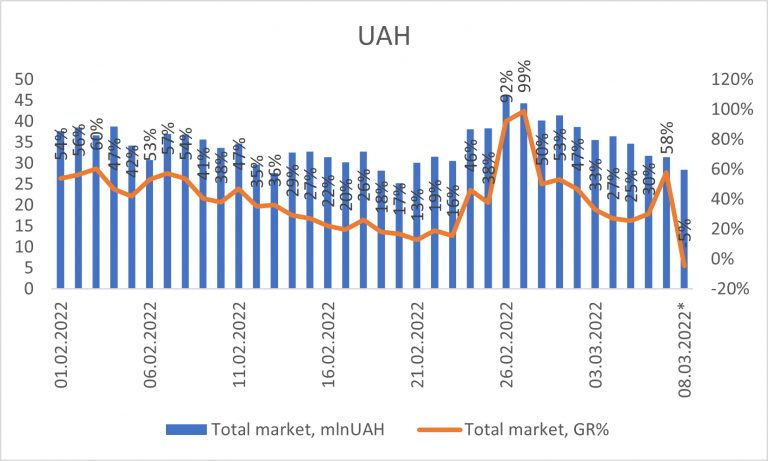

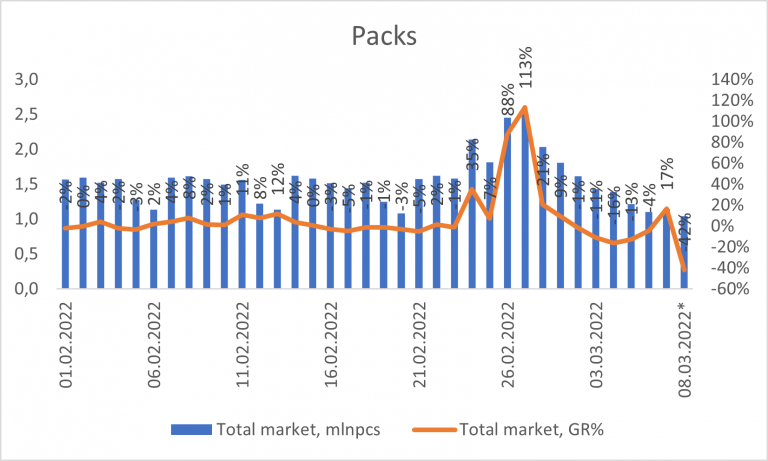

On the first day of military aggression, pharmacy sales of drugs more than doubled compared to the same day last year, and continue to grow at a high rate, although it is gradually decreasing (Fig. 1). It is related not to a decrease in demand, but to the limited number of operating pharmacies, their opening hours, limited supplies, as well as the population making a certain stock.

Fig. 1 Daily dynamics of pharmacy drug sales from 1.02.2022 to 8.03.2022.

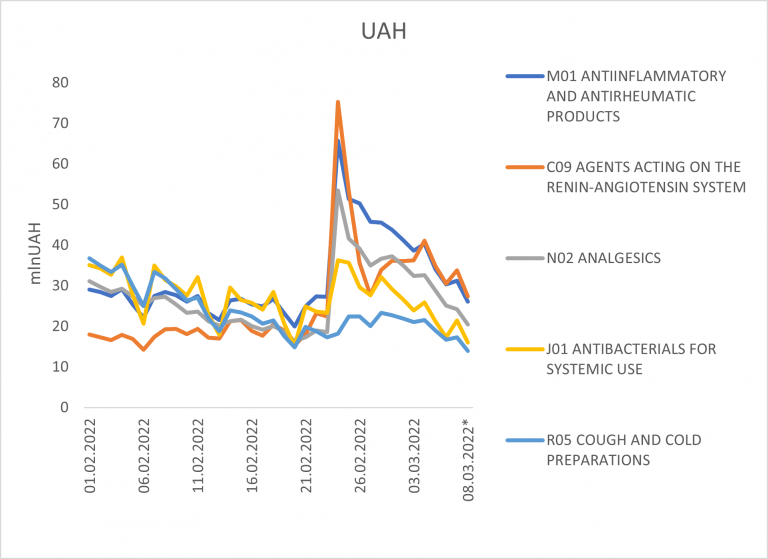

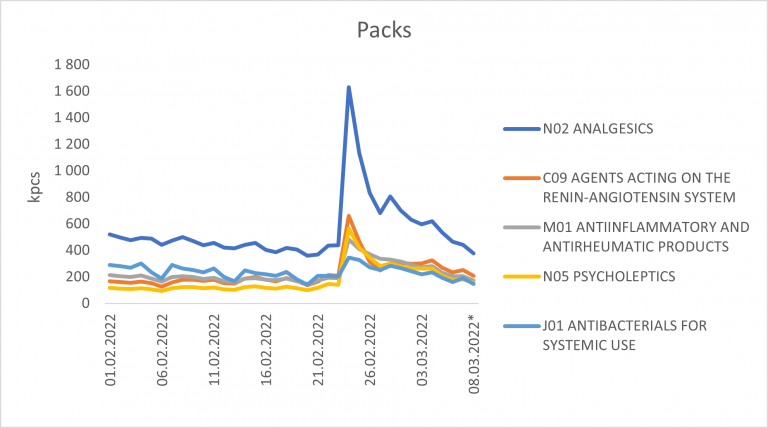

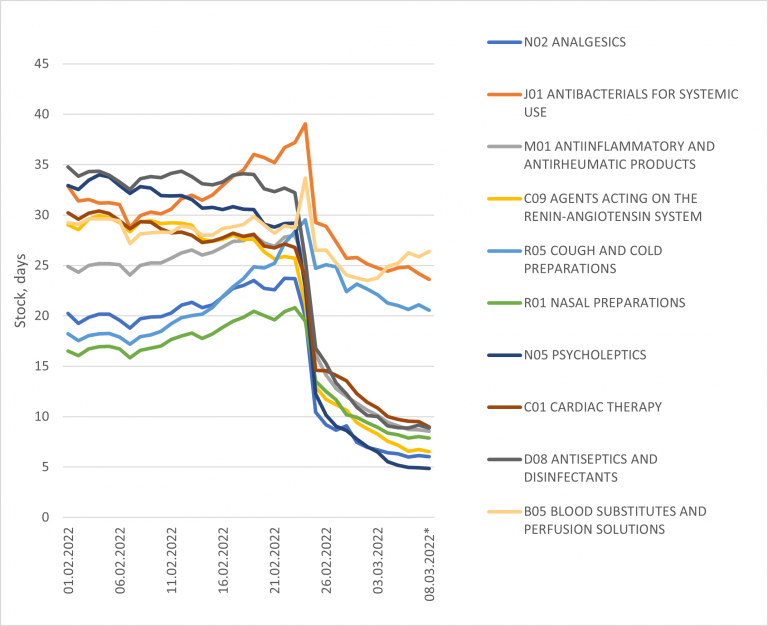

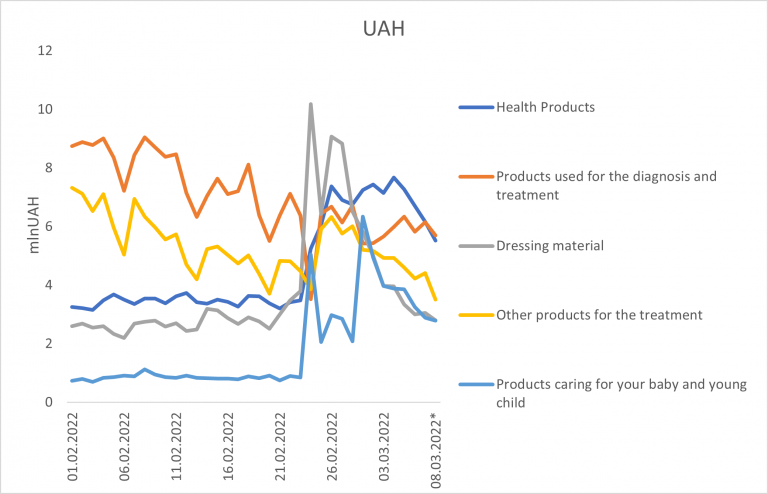

In this difficult period, the highest demand among Ukrainians was for drugs treating arterial hypertension, anti-inflammatory and cold remedies, analgesics and antibiotics, and as evidenced by volume of unit sales, psycholeptic drugs, as well as antiseptics and disinfectants (Fig. 2).

Fig. 2 Dynamics of pharmacy sales of drugs by groups of ATC classification of the 2nd tier (top 5)** from 1.02.2022 till 8.03.2022.

As for drug stocks, they are decreasing because there is information that distributors make no deliveries yet. For some ATC groups of drugs, there are stocks for less than 10 days, and their quantity continues to decrease (Fig. 3). At the same time, for some positions the state of stocks is already approaching critical.

Fig. 3 Drug stocking dynamics by ATC classification groups of tier 2 (top 10) from 1.02.2022 to 8.03.2022

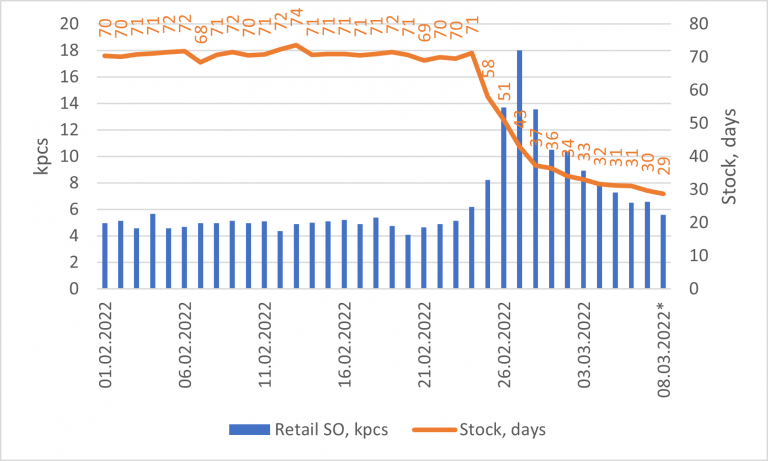

Currently, it is also important to have hemostatic agents (ATC-group B02 “ANTIHEMORRHAGIC DRUGS”). As for the volume of their pharmacy sales, they have increased several times, while the stocks in pharmacies have significantly decreased and continue to decrease (Fig. 4).

Fig.4 Dynamics of pharmacy sales volume of ATC drugs group B02 in units, and the dynamics of their stocks in pharmacies from 1.02.2022 to 8.03.2022

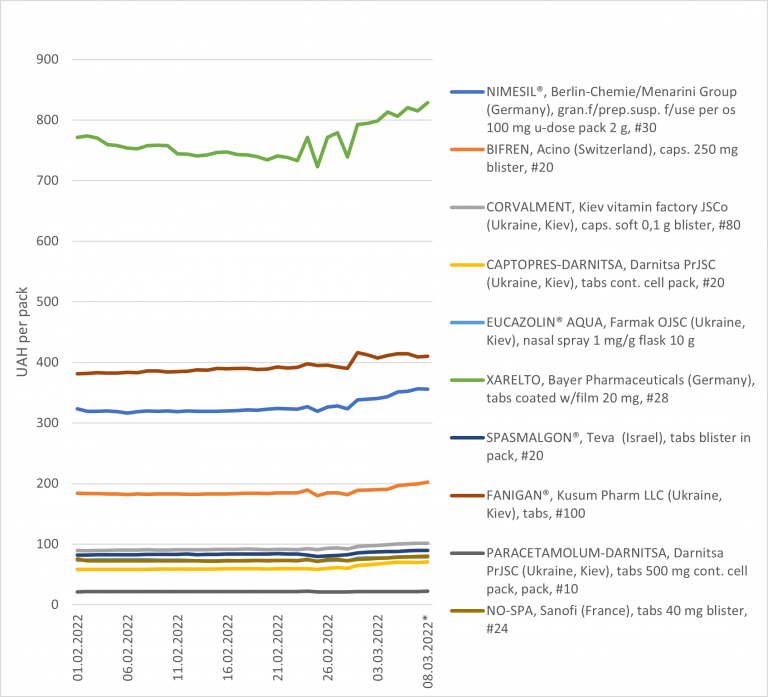

It is worth noting that, despite the increased demand for drugs and supply restrictions, there is no significant increase in prices (Fig. 5). However, price growth is still observed. Thus, for the top 10 SKUs by sales volume in monetary terms from 24.02.2022, the average price increase as of 8.03.2022 relative to the prewar period (compared to the price as of 01.02.2022) is 10%.

Fig. 5 Price dynamics for the top 10 SKUs** by sales volume in monetary terms from 1.02.2022 to 8.03.2022.

Also, at the beginning of the military aggression, the volume of sales of medical devices increased significantly, but unit sales have already shown a negative trend (Fig. 6). Which is due to the same factors as for medicines.

Fig. 6 The daily dynamics of the volume of pharmacy sales of medical devices from 1.02.2022 to 8.03.2022.

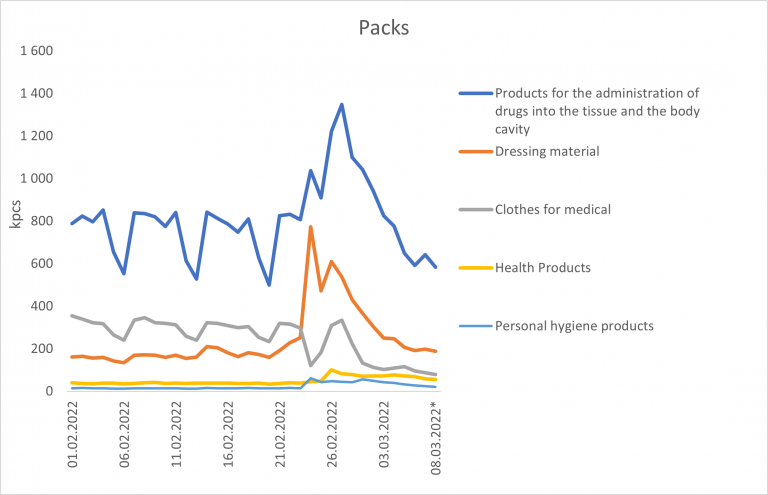

Among medical devices, the most popular are bandaging materials, nursing items, and products and components used to administer drugs and solutions into tissues and body cavities (Figure 7). There is also a significant demand for baby care products.

Fig. 7 Dynamics of pharmacy sales of medical products by subcategories** (top 5) from 1.02.2022 to 8.03.2022.

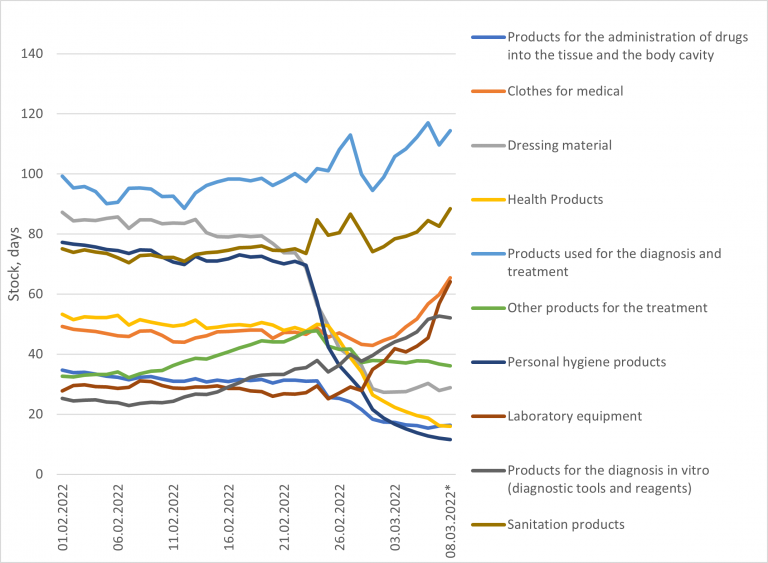

Regarding the stocks of medical devices, there is a significant decrease in the stocks of bandaging materials and personal care products (Fig. 8).

Fig. 8 Dynamics of stocks of medical devices by product subcategories (top 10) from 1.02.2022 to 8.03.2022.

Despite difficult circumstances, we continue to inform you about the state of the pharmaceutical market.

*preliminary data

**sorting by sales volume from 24.02.2022