In this article, we explore an overview of the pharmacy retail sector, its structure, and key trends. The content is based on a report by Tetiana Ivanova, Product Manager of the Market Audit Ukraine product by Proxima Research, presented at the “Online conference on technical regulations for cosmetic products.”

The initial part of the report introduced the retail pharmacy market and its structure, in particular the Ukrainian pharmacy cosmetics market in 2024.

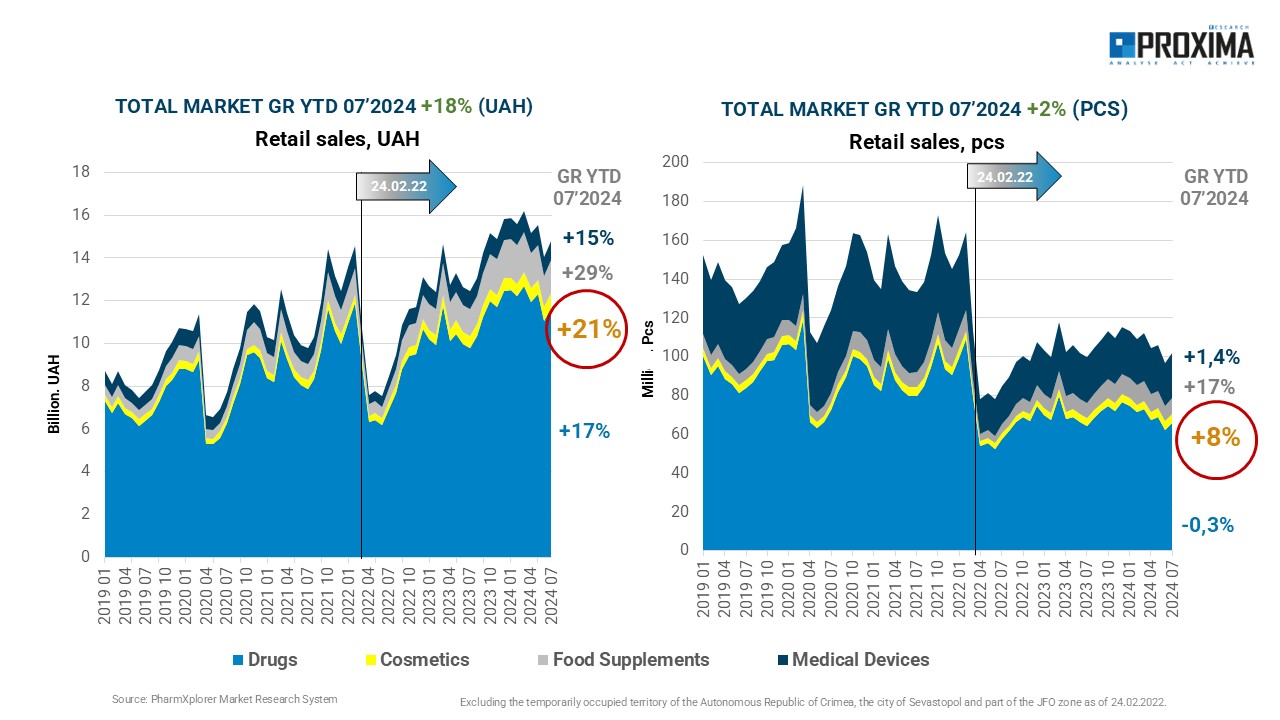

Participants were invited to examine sales dynamics in monetary terms and packages, segmented by “pharmacy basket” categories (fig. 1). Following a significant drop in volumes in February-March 2022, caused by the onset of the full-scale war, sales in monetary terms have gradually recovered and are demonstrating an upward trend. By the end of the first seven months of 2024, the total volume of the “pharmacy basket” grew by 18% in monetary terms. The cosmetics category demonstrated even stronger growth, with a 21% increase in monetary terms compared to the same period last year.

In packages, the market showed a less optimistic trend due to a substantial population decrease. However, the total volume of pharmacy retail sales in packages grew by 2% over the first seven months of 2024 compared to the same period in 2023. The cosmetics category, in particular, increased sales volumes by 8% in July 2024 compared to July 2023.

Figure 1. Retail sales volumes of “pharmacy basket” goods

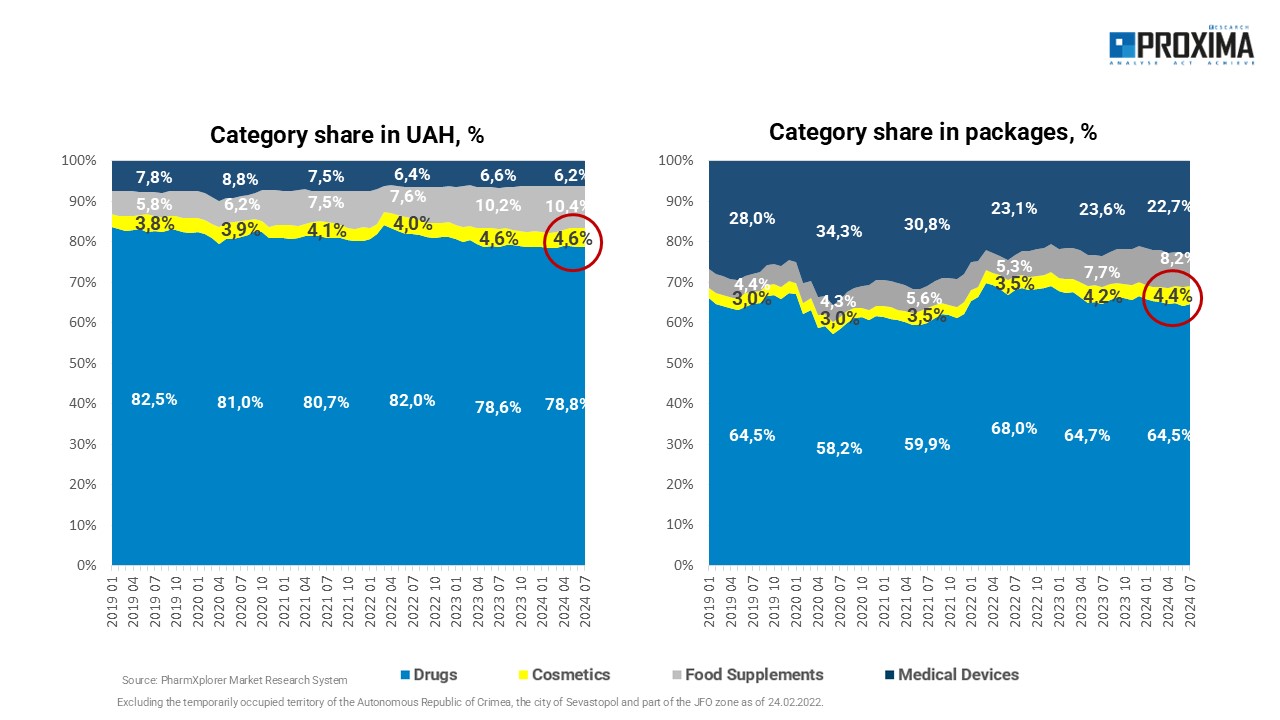

The share of the cosmetics market was also growing alongside the overall sales volumes. As of July 2024, cosmetics account for 4.6% of the “pharmacy basket” in monetary terms and 4.4% in physical terms (fig. 2).

Figure 2. Category share: monetary and physical terms

The spotlight was also placed on the online sales channel.

E-commerce in the pharmacy retail sector had its unique characteristics and was evolving at a rapid pace. In her presentation, the speaker highlighted four key categories of the “pharmacy basket”: drugs, food supplements, medical devices, and cosmetics.

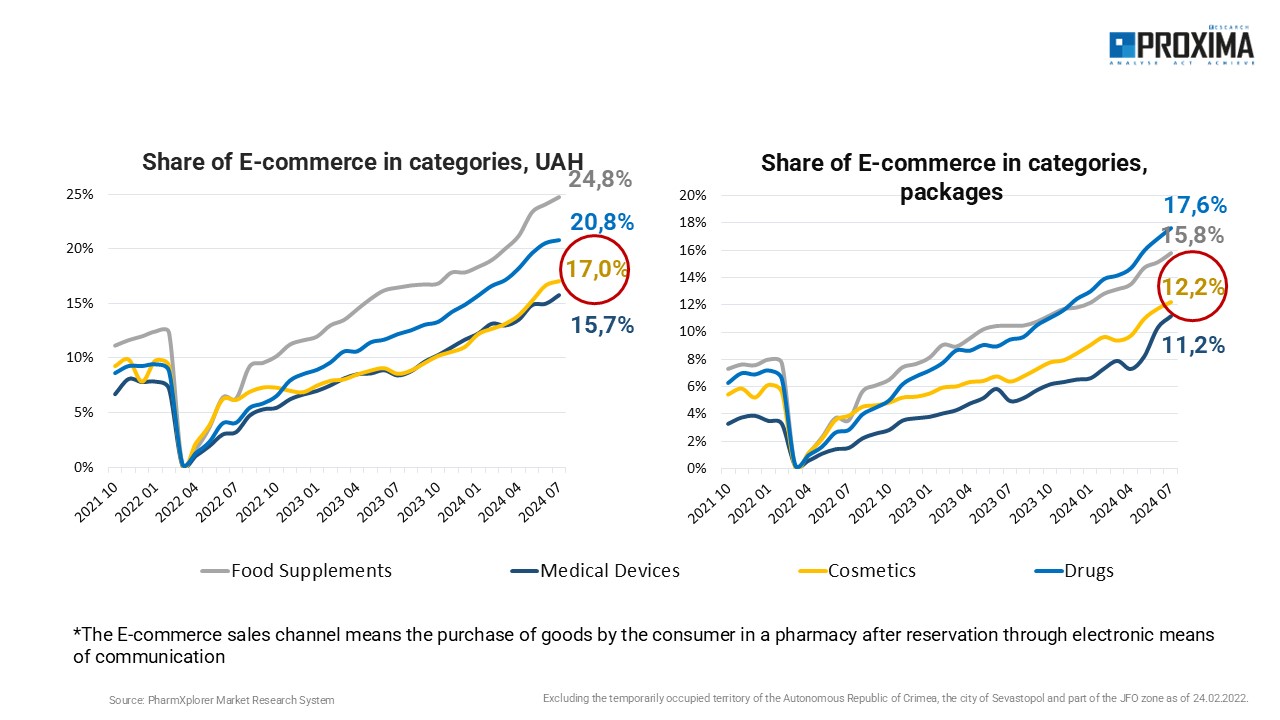

As previously mentioned, the online sales channel for cosmetics in the pharmacy retail sector continued its dynamic growth. As of July 2024, 17% of cosmetics were sold through online reservations in monetary terms, while the share in packages was 12.2% (fig. 3).

Figure 3. E-commerce share in categories: monetary and physical terms

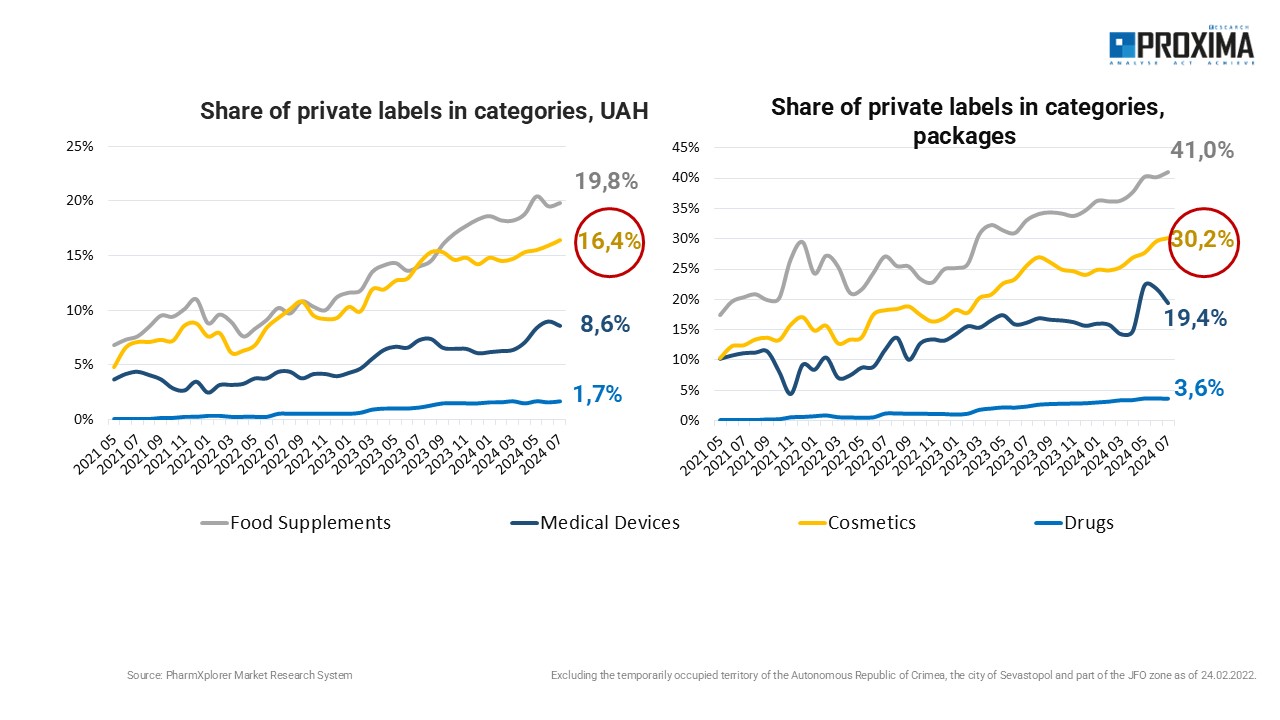

Another important trend in the pharmaceutical market was emphasized – private labels (PL).

In 2024, PLBs are actively expanding their presence in the pharmacy retail sector. Overall, their share in the “pharmacy basket” reached 4.6% in UAH and 11.4% in packages as of July 2024. For cosmetics specifically, PL accounted for 16.4% in monetary terms and 30.22% in physical terms. PL are not limited to the cosmetics category; they are also represented across other “pharmacy basket” categories, with corresponding share (fig. 4).

Figure 4. Share of PL in categories: monetary and physical terms

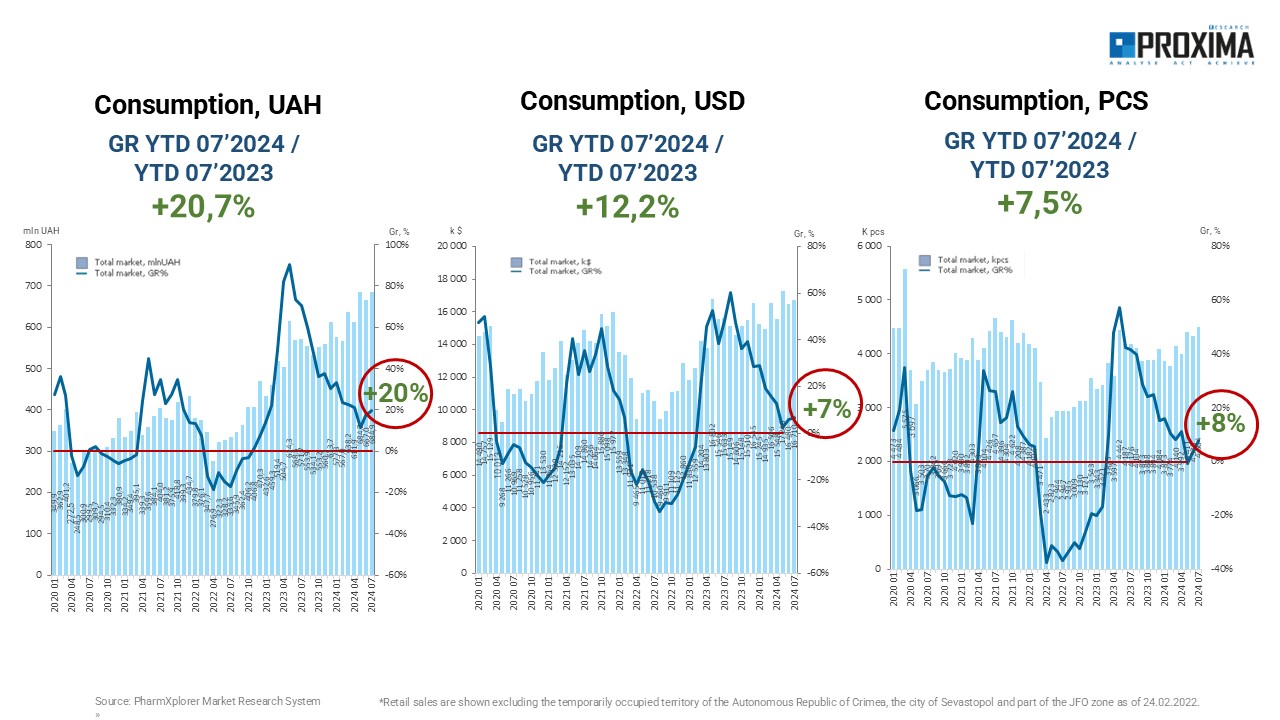

The cosmetics category within pharmacy retail showed significant growth over the first seven months of 2024. Sales increased by 20.7% in the local currency and 12.2% in USD, with packages sales rising by 7.5% compared to the same period in 2023 (fig. 5). In July 2024 alone, cosmetics demonstrated a 20% increase in sales in monetary terms (UAH), 7% in USD, and an 8% rise in physical terms compared to July 2023.

Figure 5. Cosmetics consumption: monetary and physical terms

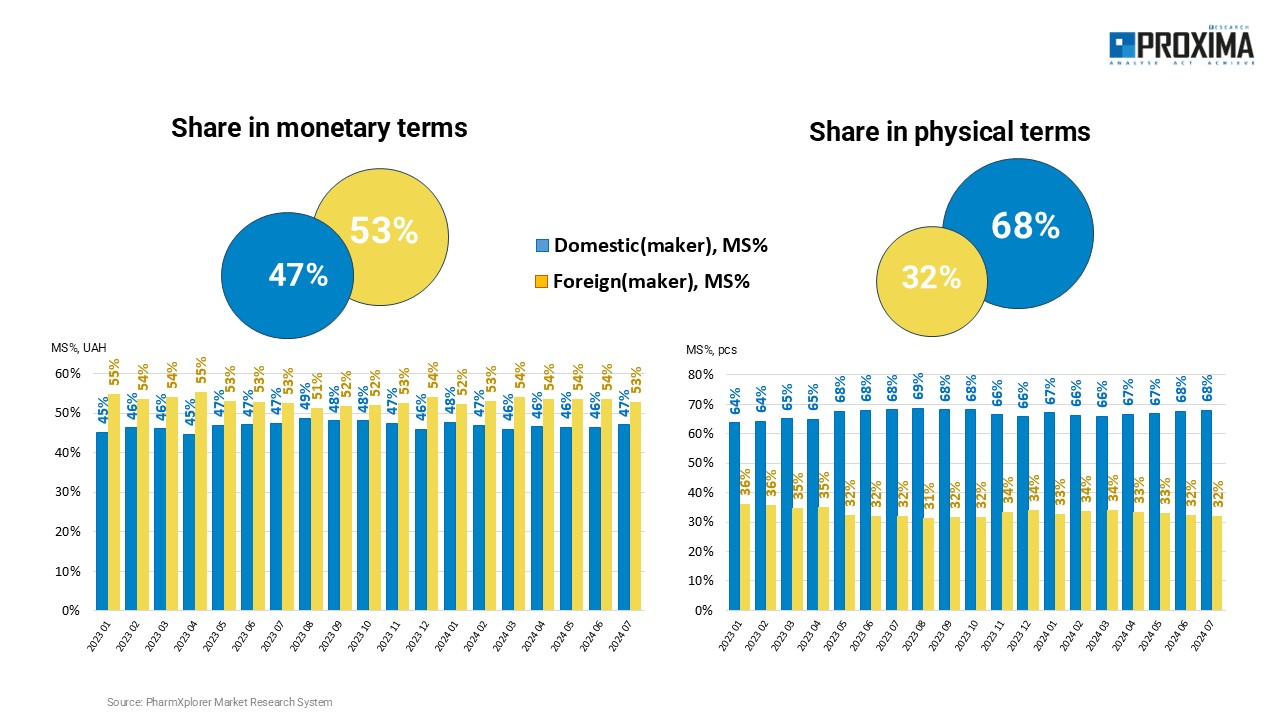

The share of domestic cosmetics manufacturers accounts for 47% in monetary terms, while imported products hold 53%. In physical terms, domestic manufacturers represent 68%, leaving imported products with just 32% (fig. 6). This distribution reflects how the economic situation in Ukraine drives increased demand for locally produced goods.

Figure 6. Share of domestic and foreign manufacturers in the Ukrainian market

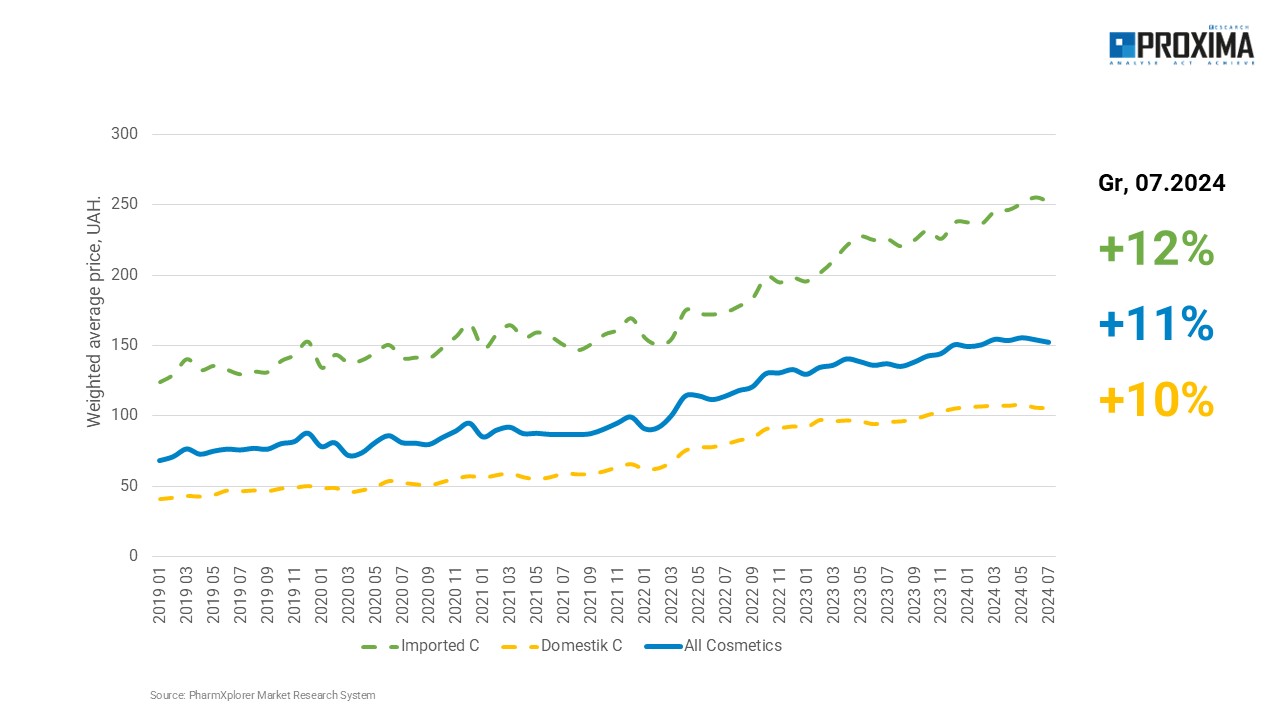

In July 2024, compared to July 2023, the weighted average price of domestic cosmetics increased by 10% in hryvnias, while imported cosmetics showed an average price increase of 12% (fig. 7).

Figure 7. Dynamics of the weighted average price for domestic and imported cosmetics

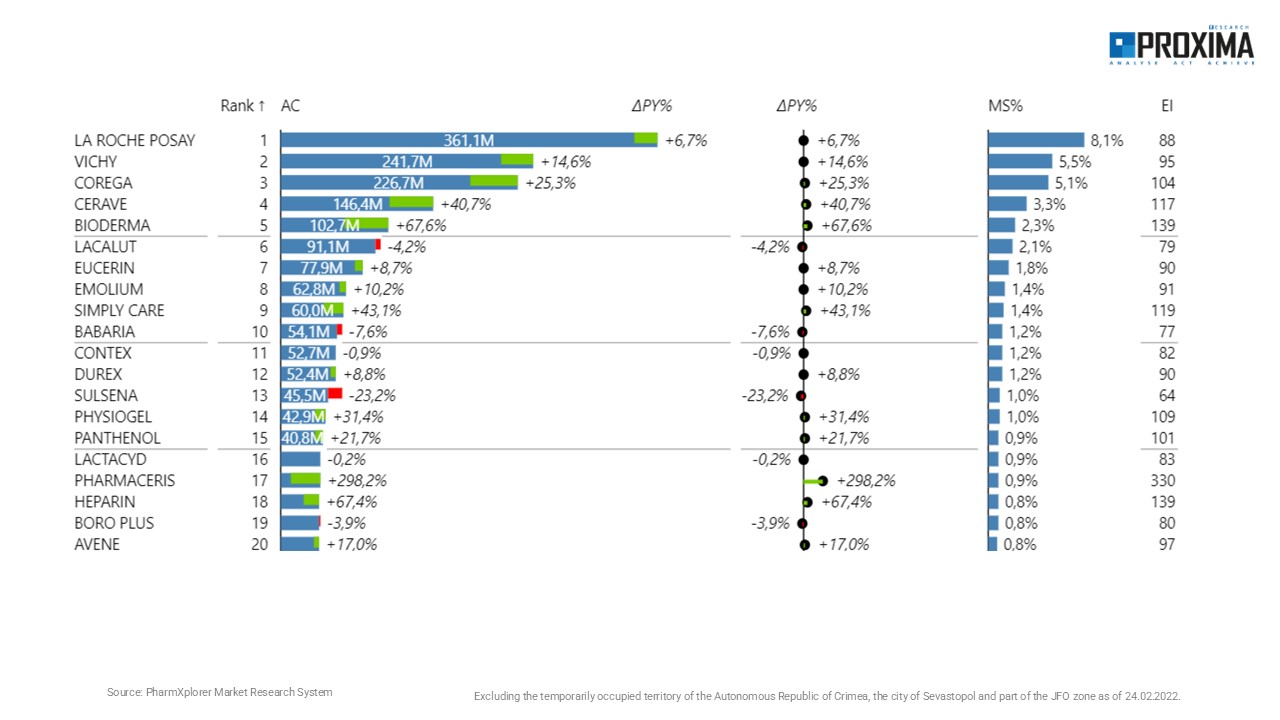

In the context of brand representation within the cosmetics category in pharmaceutical retail, this category has its unique characteristics and differs significantly from the cosmetics segment in the FMCG sector. The slide presents the TOP-20 brands for the first seven months of 2024 in monetary terms, showing their market share, growth, and evolution index (fig. 8).

Leaders include LA ROCHE POSAY, VICHY, COREGA, and CERAVE. Interestingly, even among the TOP-5 brands, there are representatives from various subcategories within the cosmetic products segment in pharmaceutical retail.

Figure 8. Brand ranking in the retail market. YTD 07.2024, UAH

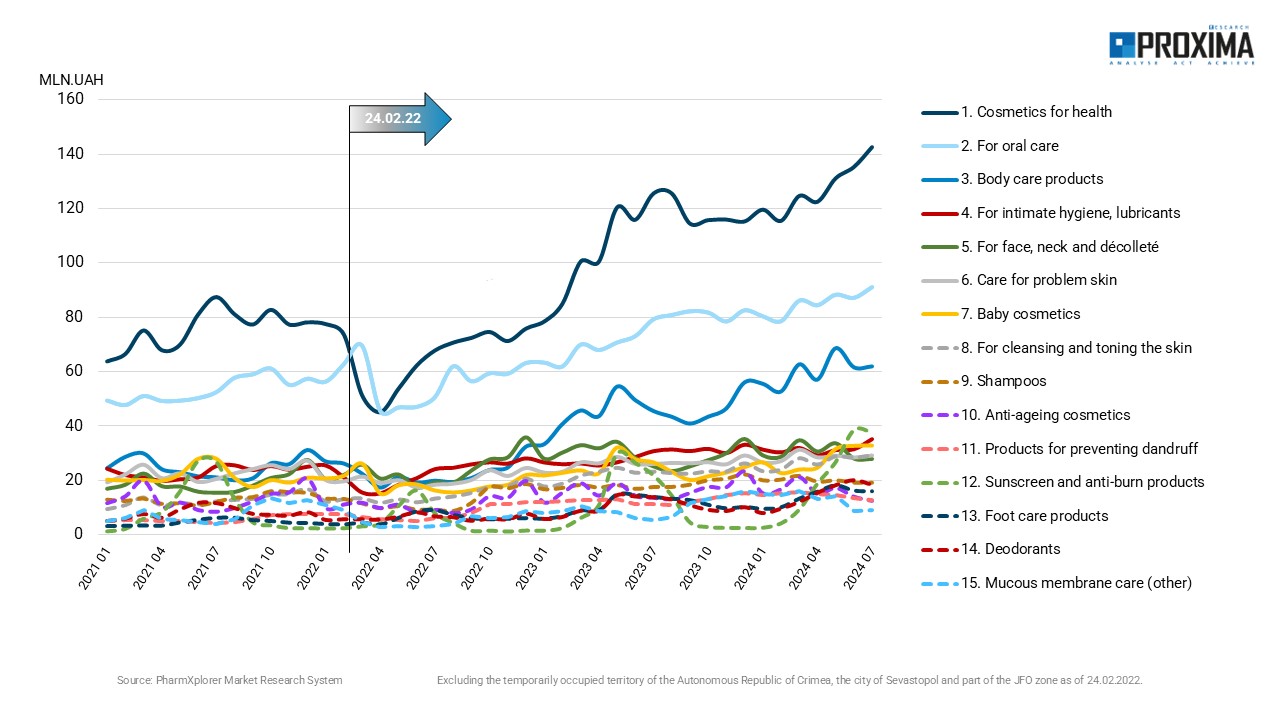

Regarding the assortment of cosmetic products in the pharmaceutical retail market, subcategories of cosmetic items are presented on the slide (fig. 9). The leading category in pharmaceutical retail is health-oriented cosmetic products, which is logical since people primarily visit pharmacies for products aimed at improving health. However, other categories are also in demand, such as oral care products, body care products, intimate hygiene products, and lubricants. In fifth place are products for facial, neck, and décolleté care—items typically associated with FMCG retail outlets.

Figure 9. Top-15 leading second-level categories of cosmetics in UAH based on MAT2024’07 results

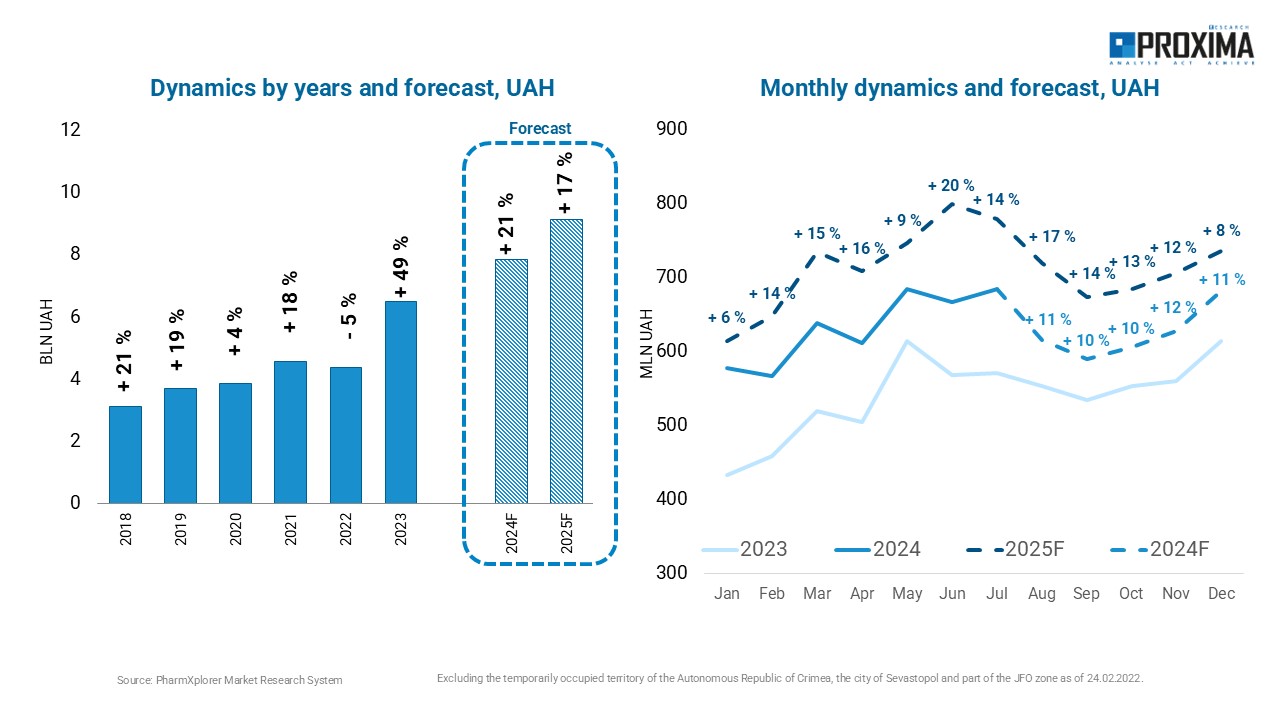

In conclusion, we would like to share a positive note with analytical forecast from Proxima Research. As of the first seven months of 2024, the cosmetics market in the pharmaceutical retail sector demonstrated growth of 20.7% in UAH, 12.2% in USD, and 7.5% in packages. Projections for 2025 indicate that the cosmetics market will continue to grow, with an expected increase of 17%.

The graph also displays the monthly forecast dynamics for 2024–2025 (fig. 10). Notably, in 2024, Proxima Research introduced a new dashboard format on the Power BI platform, allowing data to be displayed in two formats: a solid line for recorded results and a dashed line for forecasted figures.

We anticipate that the cosmetics sector will show a positive growth trend in the second half of the year, with a 10–11% increase in monetary terms. Moreover, robust growth is also forecasted for 2025.

Figure 10. Forecast for the retail cosmetics market development in Ukraine from August 2024 in UAH

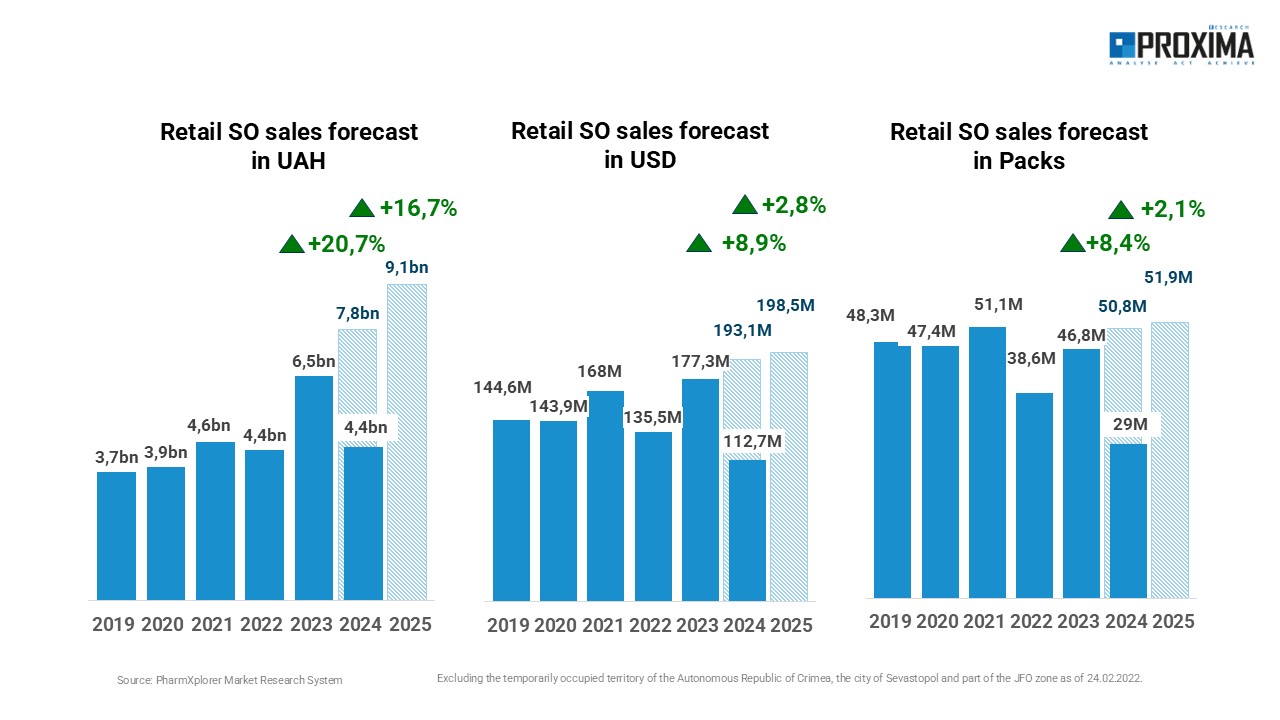

As for the forecast for the development of the retail cosmetics market: in hryvnia, we forecast growth of 20.7% in 2024 and 16.7% in 2025; in dollar terms, the growth will be 8.9% in 2024 and 2.8% in 2025. We also forecast positive growth dynamics in sales of cosmetics in packages: in 2024, the growth will be 8.4%, and in 2025 – 2.1% (fig. 11).

Figure 11. Forecast for Ukrainian retail cosmetics market development amid war

Summarizing the above, the following key aspects characterize the state of the retail cosmetics market in Ukraine in 2024:

We forecast that in the second half of 2024, cosmetics will show growth at a level of 10-11% in monetary terms, with active category expansion expected in 2025.

Order a presentation of the Proxima Research Audits product.

By clicking the “Subscribe” button, you consent to the processing of personal data and the receipt of electronic messages about Proxima Research products and services, and you agree to our Terms of Use. Your data will be processed in accordance with our Privacy Policy. You can unsubscribe at any time.

or