Kazakhstan is one of the key players in the Central Asian pharmaceutical market. Its significance is determined not only by the scale of its territory but also by its high growth potential, driven by several factors: population growth, rising prosperity, expanding need for medical treatment, and the growing prevalence of chronic diseases, which directly impacts the sales of drugs and dietary supplements in Kazakhstan.

An additional driver is government initiatives for healthcare infrastructure development.

This publication presents an overview of the key indicators and trends of the retail pharmaceutical market of the Republic of Kazakhstan (covering sales of drugs and dietary supplements in Kazakhstan) for Q1 2025, with a focus on potential growth points and areas of concern for market participants.

The material was prepared based on data from the market research analytical system “PharmXplorer” by “Proxima Research International”.

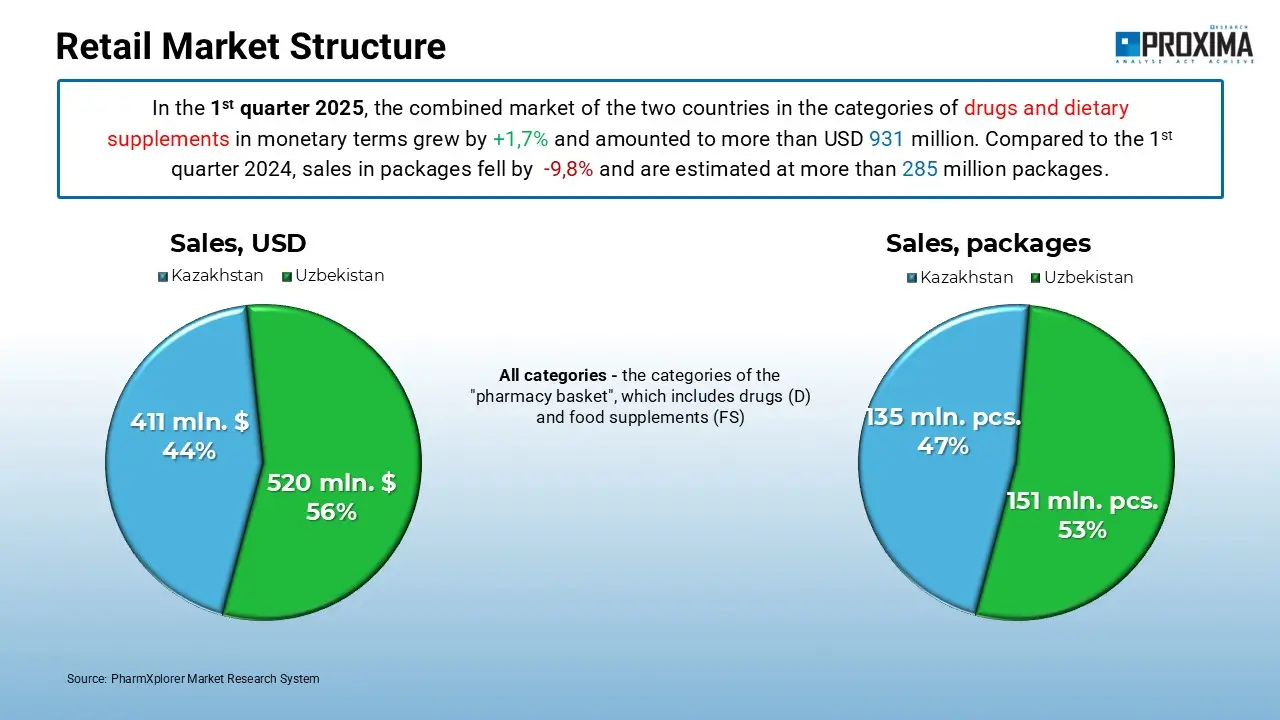

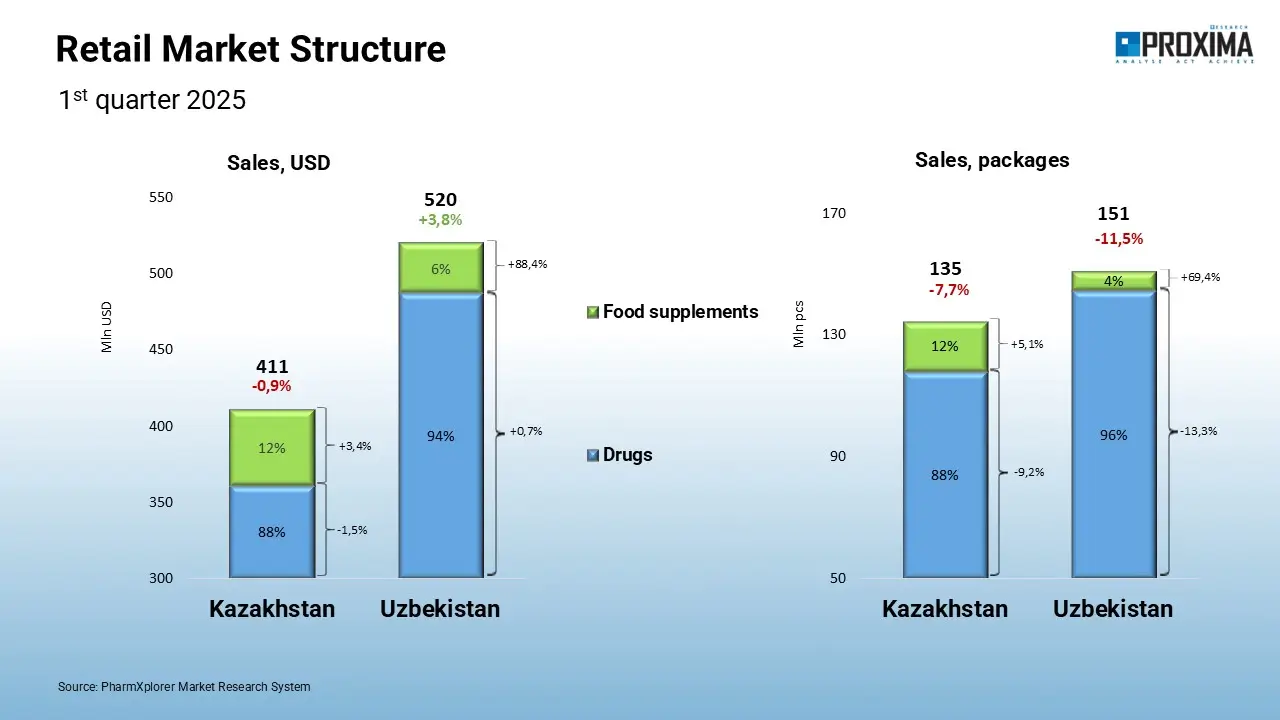

In Q1 2025, the volume of the retail pharmaceutical market in Kazakhstan reached 411 million USD in monetary terms and 135 million packages in physical terms (Fig. 1). Compared to the neighboring state, the Republic of Uzbekistan, both indicators are lower, which can be explained by Kazakhstan’s smaller population despite its significantly larger territory.

Fig. 1. Volume of the retail pharmaceutical market of the Republic of Kazakhstan in comparison with the Republic of Uzbekistan as of Q1 2025.

Compared to the same period of the previous year, the sales volume of drugs and dietary supplements in the pharma market of Kazakhstan in monetary terms remained almost unchanged, decreasing by only 0.9%, whereas in physical terms, a decline of 7.7% was observed (Fig. 2). Compared to Uzbekistan, the pharmacy market in Kazakhstan shows a milder downturn. The main contribution to consumption is made by drugs – 88% in both monetary and physical terms.

Fig. 2. Structure and volume of the retail pharmaceutical market of the Republic of Kazakhstan as of Q1 2025 in comparison with the Republic of Uzbekistan.

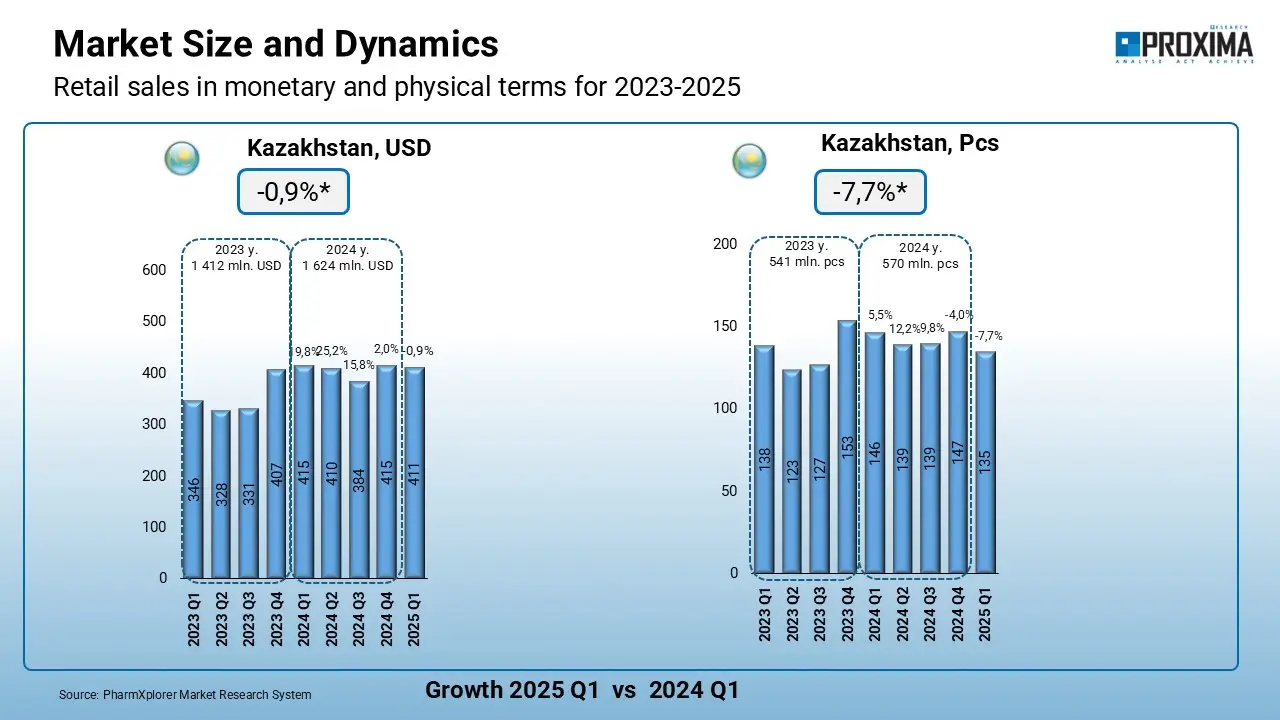

Overall, the Kazakhstan pharma market demonstrates stability, without sharp fluctuations in consumption indicators (Fig. 3).

Fig. 3. Dynamics of the retail pharmaceutical market of the Republic of Kazakhstan from Q1 2023 to Q1 2025.

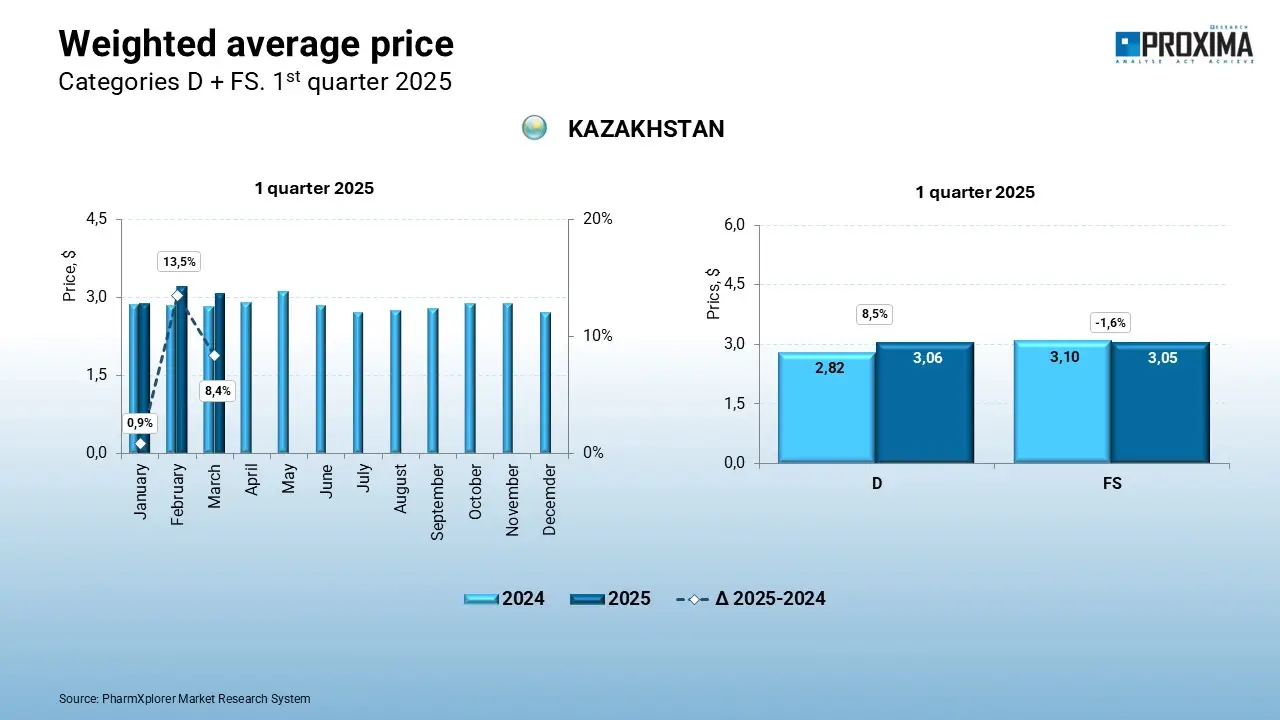

The weighted average retail price of one package of drugs category in Q1 2025 shows a growth of 8.5%, while the dietary supplements segment recorded a decrease of 1.6% (Fig. 4).

Fig. 4. Dynamics of the weighted average price of one package in the pharma market of the Republic of Kazakhstan from 2024 to Q1 2025.

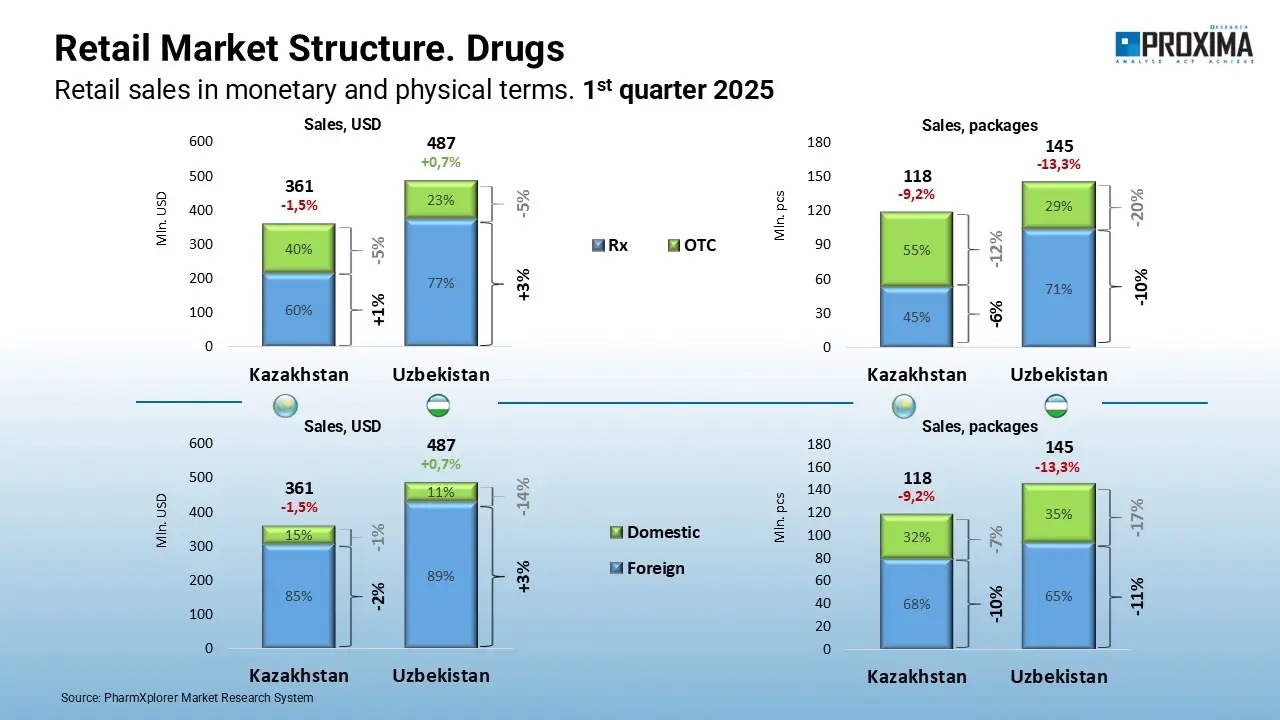

Structure of the pharmaceutical market by prescription drugs status is quite balanced: 60% of sales in monetary terms are from prescription drugs and 45% from over-the-counter drugs (Fig. 5). In terms of the country of origin, the situation is different: imported drugs prevail, especially in monetary terms – 85% – while in packages their share is smaller – 68%. This may indicate that domestic manufacturers are mainly concentrated in the segment of less expensive drugs, ensuring economic accessibility for the population.

Fig. 5. Structure of the retail pharma market of the Republic of Kazakhstan in Q1 2025 by prescription status, as well as domestic and foreign manufacturers, and comparison with the Republic of Uzbekistan.

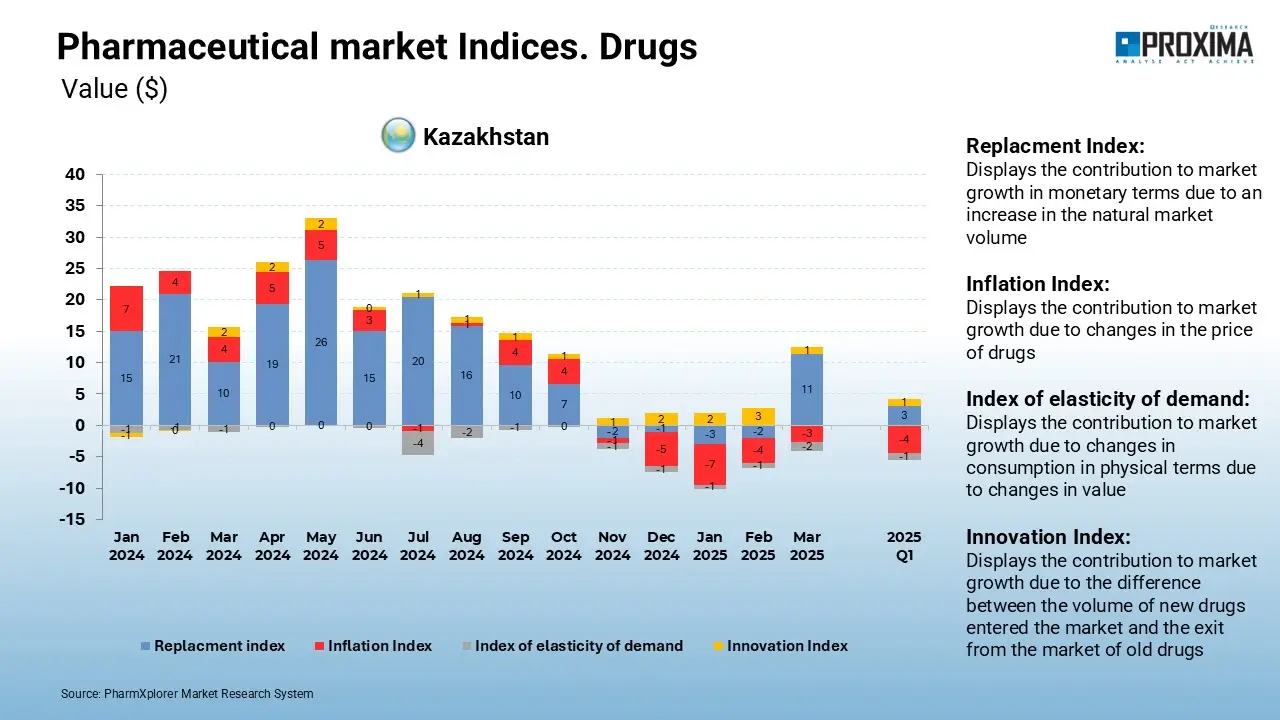

The growth of the medicinal products market in monetary terms during the reviewed period was due to substitution and the appearance of new drugs, which indicates that market development is driven by assortment renewal rather than price growth (Fig. 6).

Fig. 6. Indices of sales volume change for medicinal products in the Republic of Kazakhstan from January 2024 to April 2025.

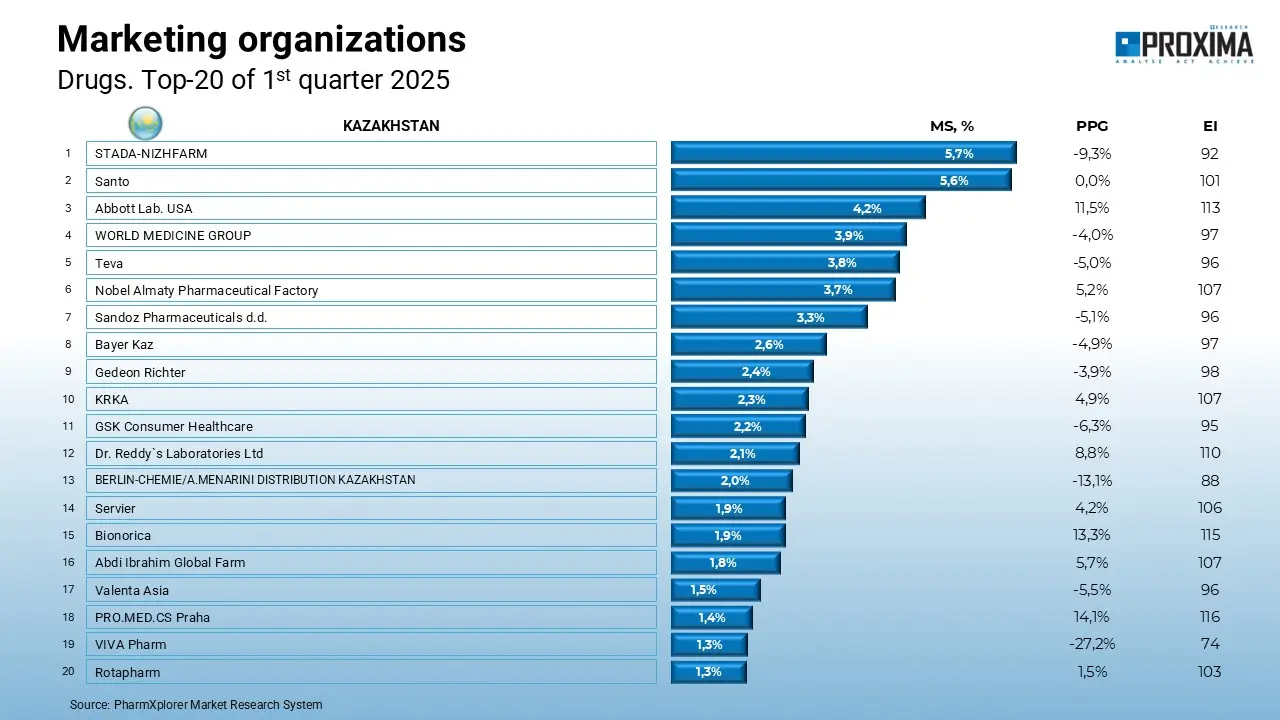

International players maintain leading positions drugs market of the Republic of Kazakhstan. The ranking of marketing organizations in Q1 2025 was led by Stada-Nizhpharm, Santo, and Abbott Laboratories (Fig. 7).

Fig. 7. Top 20 marketing organizations by retail sales volume of medicinal products in monetary terms in the Republic of Kazakhstan as of Q1 2025.

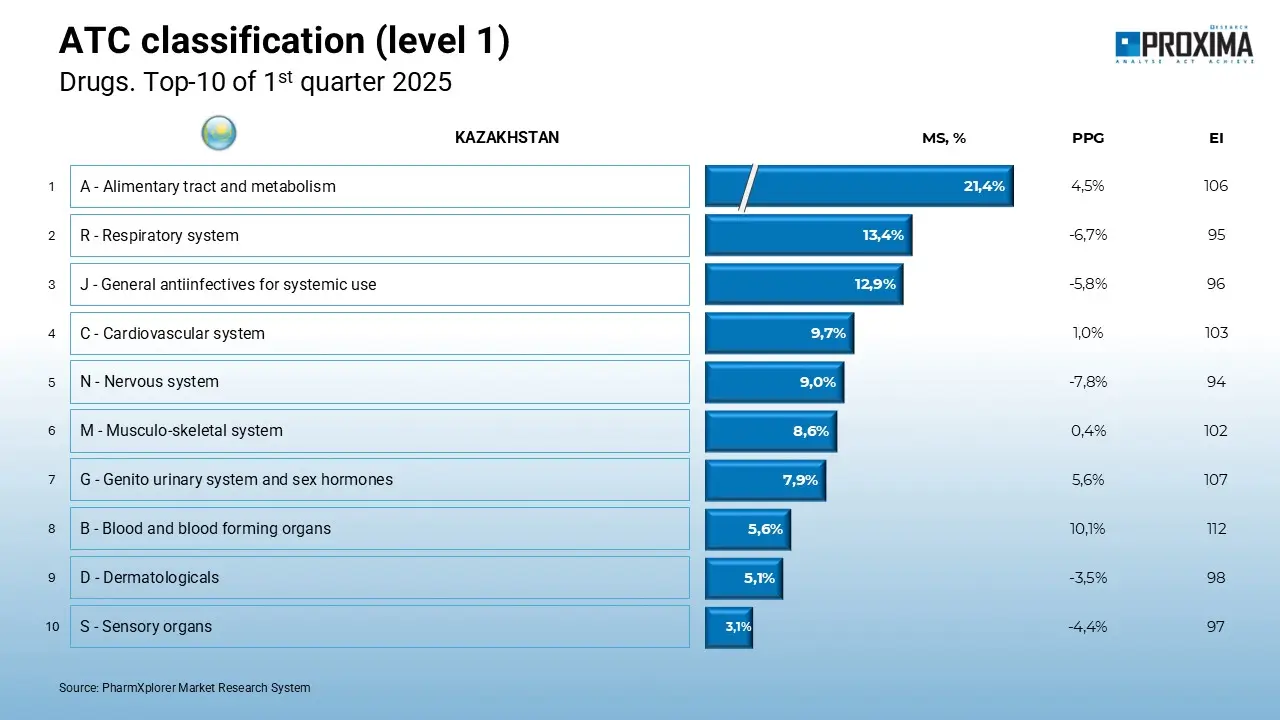

The largest sales volume is generated by agents affecting the digestive system and metabolism, those acting on the respiratory system, and antimicrobials for systemic use (Fig. 8).

Fig. 8. Top 10 groups of drugs by ATC classification level 1 by retail sales volume in monetary terms in the Republic of Kazakhstan as of Q1 2025.

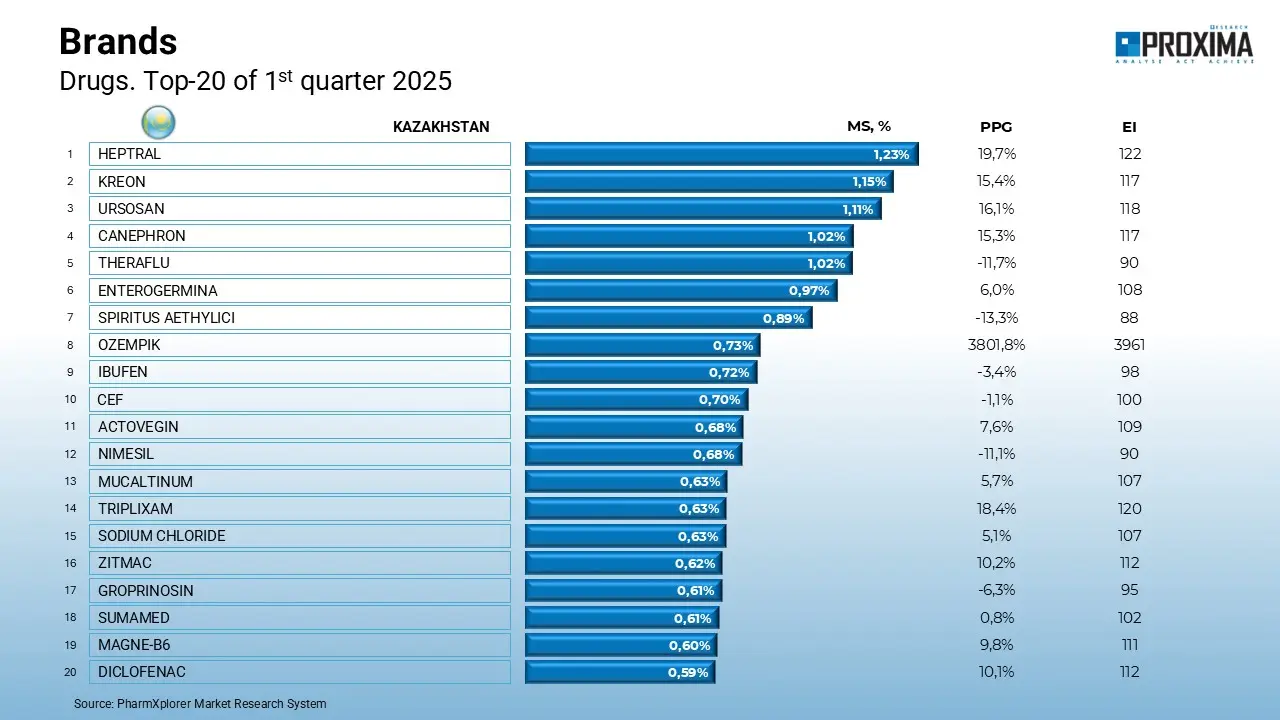

The ranking of drug brands was topped by Heptral, Creon, and Urosan (Fig. 9).

Fig. 9. Top 20 brands of medicinal products by retail sales volume in monetary terms in the Republic of Kazakhstan as of Q1 2025.

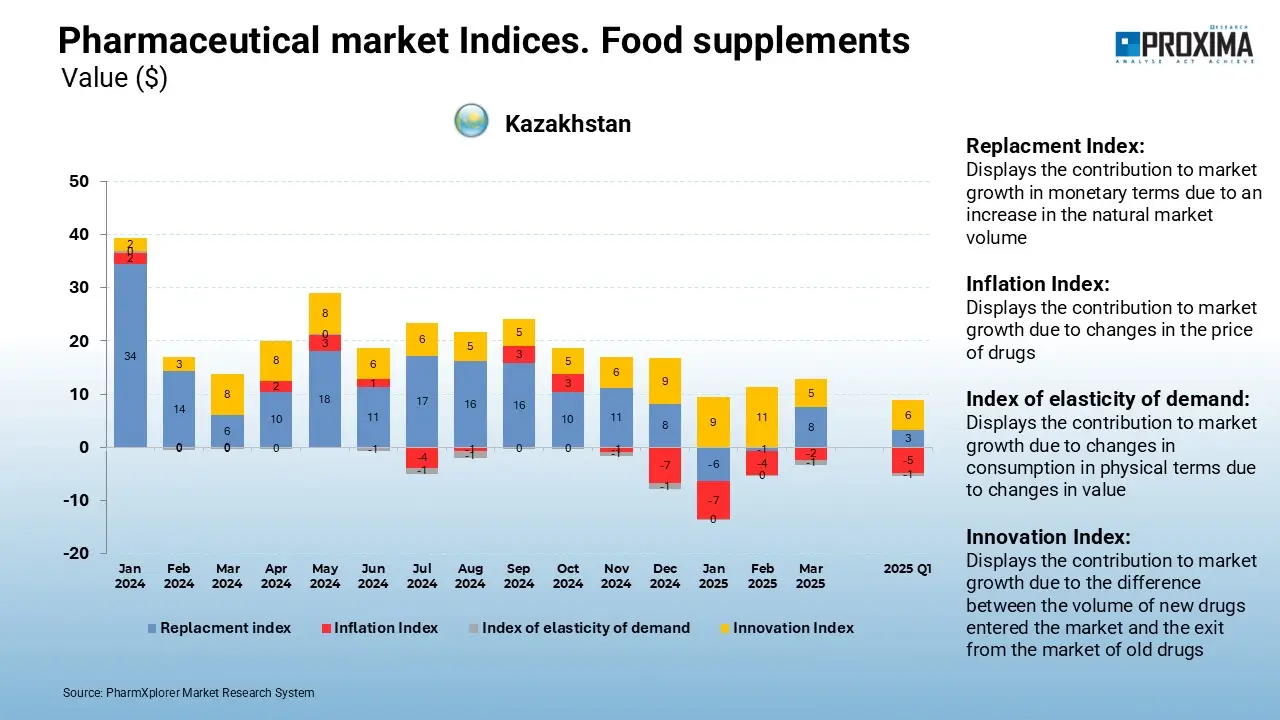

The growth of the dietary supplements market was also driven by substitution and the appearance of new products, but the contribution of the innovation factor is higher compared to drugs (Fig. 10).

Fig. 10. Indices of sales volume change for dietary supplements in the Republic of Kazakhstan from January 2024 to April 2025.

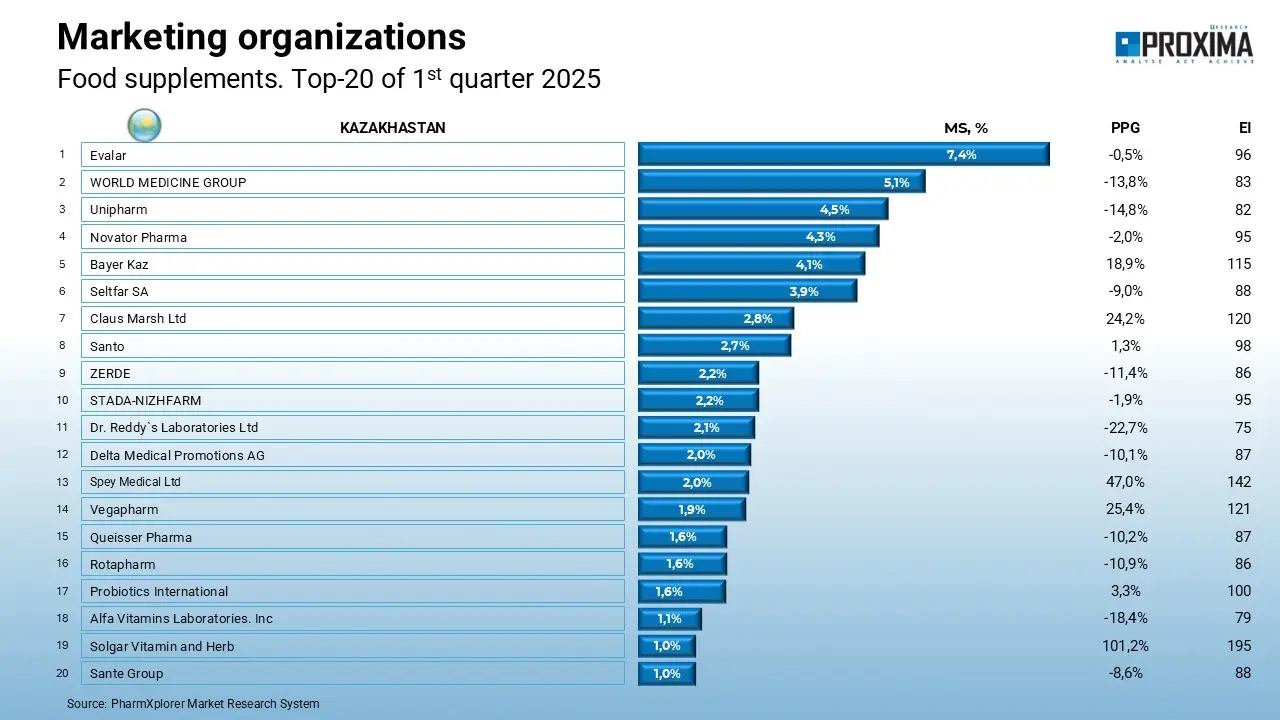

Among marketing organizations in this market, Evalar, World Medicine, and Unipharm are dominant (Fig. 11).

Fig. 11. Top 20 marketing organizations by retail sales volume of dietary supplements in monetary terms in the Republic of Kazakhstan as of Q1 2025.

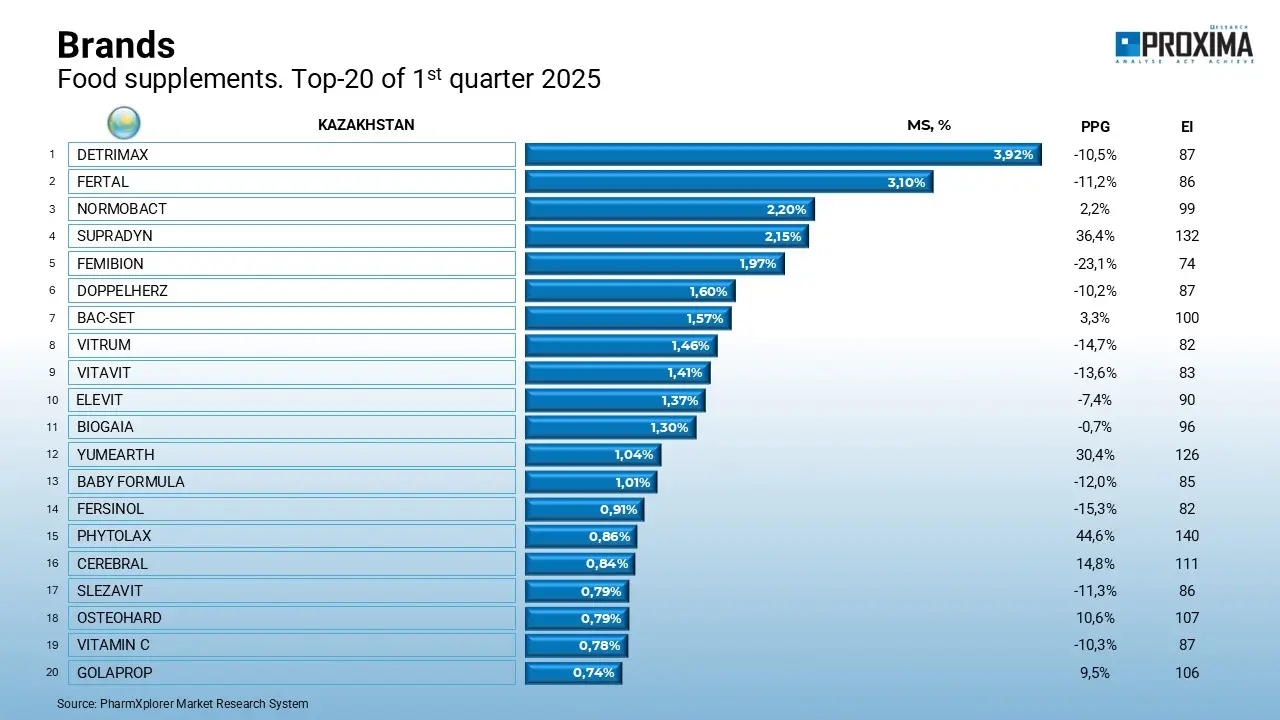

And among brands – Detrimax, Fertal, and Normobact (Fig. 12).

Fig. 12. Top 20 brands of dietary supplements by retail sales volume in monetary terms in the Republic of Kazakhstan as of Q1 2025.

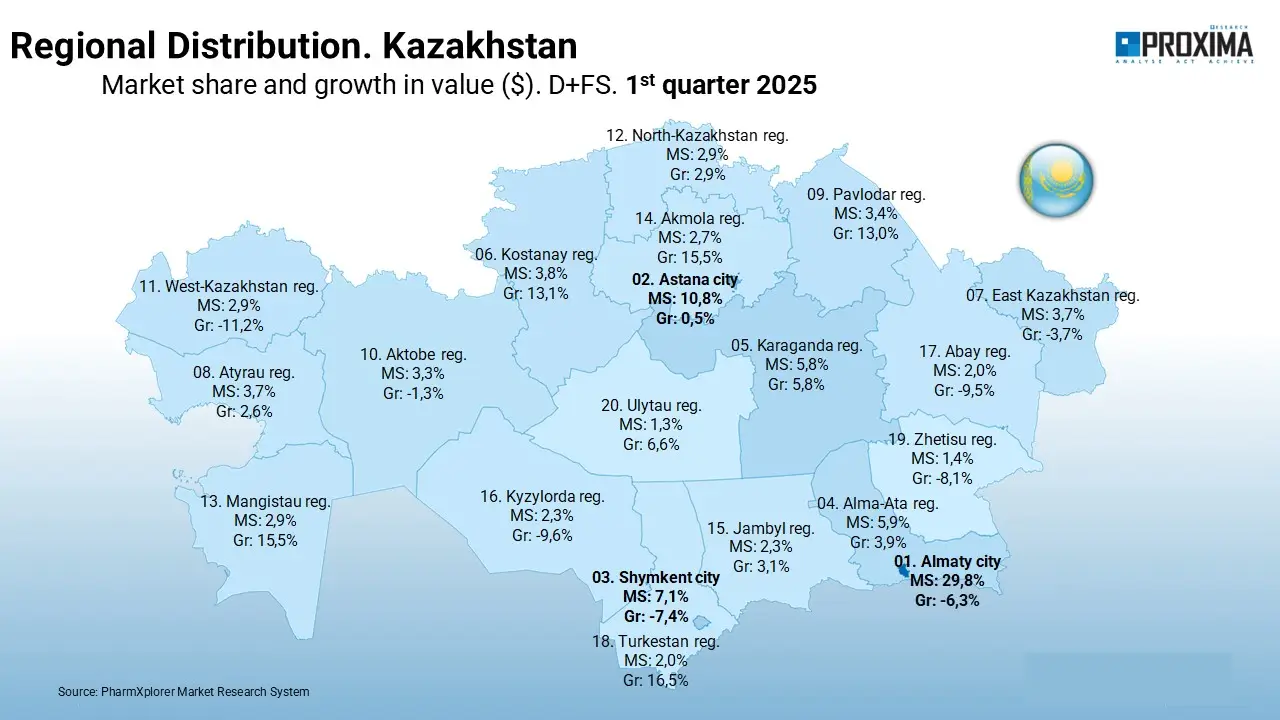

The maximum retail sales volume of drugs and dietary supplements in Kazakhstan is concentrated in two cities – Almaty (the largest city and former capital) and Astana (the current capital). At the same time, some regions show double-digit growth rates (e.g., Mangistau, Pavlodar, Kostanay, Akmola regions), which indicates the potential for development in these territories (Fig. 13).

Fig. 13. Regional distribution of consumption volumes of drugs and dietary supplements in the Republic of Kazakhstan as of Q1 2025.

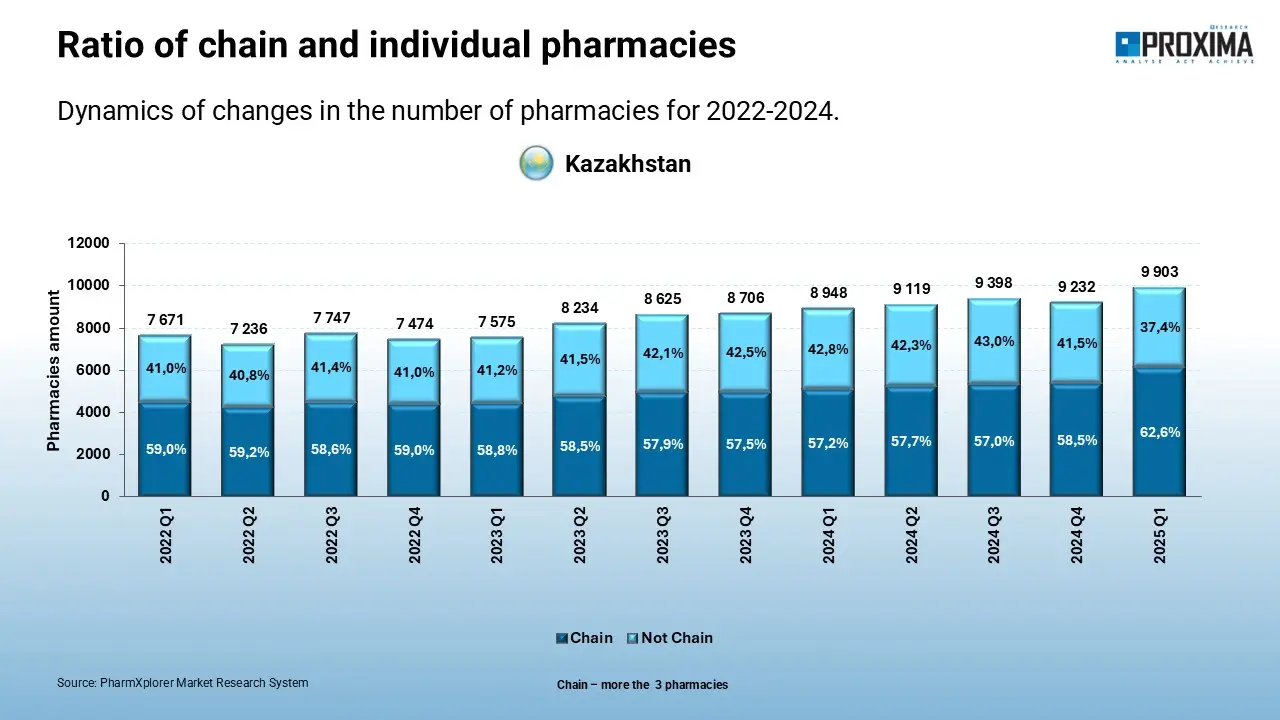

The share of pharmacy chains in the Republic of Kazakhstan continues to grow, reaching 62.6% in Q1 2025, posing increasing competition to individual pharmacies (Fig. 14).

Fig. 14. Ratio of chain and individual pharmacies in the Republic of Kazakhstan in dynamics from Q1 2022 to Q1 2025.

The pharmaceutical market of the Republic of Kazakhstan remains relatively stable, maintaining predictability for strategic decisions, which creates favorable conditions for planning long-term investments. In Q1 2025, consumption volume in monetary terms remained almost unchanged (-0.9%), but a decline was noted in packages (-7.7%). Market development in the reviewed period is driven not by price growth, but by consumption substitution and the appearance of new products (especially in the dietary supplements segment). This may indicate that new products are finding demand, but so far in limited volumes, given price sensitivity.

At the same time, the market is characterized by a high dependence on imported drugs, which means significant reliance on foreign supplies. As the drug sales analysis in Kazakhstan showed, this poses a challenge to the sustainability and security of the country’s drug supply.

The regional sales structure highlights the market’s concentration in the largest cities — Almaty and Astana, where the main purchasing activity and developed infrastructure are focused, as confirmed by pharmacy sales statistics. At the same time, demand growth in several regions with double-digit rates shows the potential for market expansion into less developed territories, opening up prospects for investors and marketers focused on regional expansion.

The increase in the share of chain pharmacies to 62.6% in Q1 2025 indicates ongoing market consolidation and increased competition.

Accurate data is essential for making informed strategic decisions. Proxima Research offers Audits for Pharma Companies, customized analytical reports, and interactive dashboards for the pharmaceutical sector.

Order a detailed pharmaceutical market analysis of your products or competitive drug niches in Kazakhstan, Uzbekistan, and Ukraine. Find growth points for your business!

Contact us to receive a personalized offer.

If the topic of the article caught your interest — leave a request. We’ll discuss how this can work for you.

By clicking the “Submit Application” button, you consent to the processing of personal data and to receiving electronic messages about Proxima Research products and services, and you agree to our Terms of Use. Your data will be processed in accordance with our Privacy Policy. You may unsubscribe at any time.

By clicking the “Subscribe” button, you consent to the processing of personal data and the receipt of electronic messages about Proxima Research products and services, and you agree to our Terms of Use. Your data will be processed in accordance with our Privacy Policy. You can unsubscribe at any time.

or