The pharmaceutical industry plays a key role in today’s world, providing humanity with safe and effective medicines and driving science, the economy and the healthcare system forward. It is at the same time a driver of innovation and a socially significant sector where the balance between business interests and the interests of society is particularly important.

In this article we offer readers a review of global trends in the pharmaceutical business. We will consider the development trends of the global medicines market as a whole, and also take a closer look at three of its major segments — the American, the European and the Central Asian.

The role of AI in the pharmaceutical business today is strategic and transformative. It accelerates the process of creating new medicines, reduces costs, and increases the accuracy of decisions in many areas — from research and development (R&D) to marketing and logistics.

Areas of application in the pharma business:

Thus, the use of AI in the pharmaceutical industry accelerates research, reduces development costs, improves safety and access to therapy, and strengthens the personalisation of treatment.

The industry’s focus is shifting from “universal” medicines to targeted and personalised approaches. Therapies based on genetics and cells are becoming increasingly widespread — CAR-T, gene editing, mRNA platforms.

Personalised medicine using biomarkers and genomic data helps create more effective and safer medicines. This is beneficial both for patients (better outcomes) and for pharmaceutical companies (competitive advantage and premium product categories).

Given the turbulent times and the high degree of uncertainty about how events in the world will develop further, the attention of pharma business representatives is focused on strengthening resilience and optimising supply chains. After the COVID-19 pandemic and geopolitical events (for example, tariffs and trade restrictions), companies are gradually moving to more resilient and flexible logistics, strengthening supply chains, including through localisation of production and the use of digital platforms for forecasting and tracking.

A wave of cooperation between large pharmaceutical and biotechnology companies continues, especially in Asia and China. Mergers and acquisitions strengthen drug portfolios. This helps major players expand access to innovation and diversify risks.

As an increasing number of costly treatment methods appear on the market, the topic of pricing of medicines remains in the spotlight for patients and the media.

In the USA, pricing reforms and pressure on medicine manufacturers are intensifying, including agreements to reduce prices. In Europe, discussion of regulation of innovation and the competitiveness of the industry is growing, which may affect local R&D strategies.

Regulators are reconsidering the balance between access to medicines and stimulation of scientific innovation.

Thus, the pharma business is moving towards innovation, personalisation and prevention, actively using digital technologies and biotechnologies to create new, more effective medicines.

Next, we will consider the main indicators and development trends of the global pharmaceutical market.

The global market for pharmaceutical products (prescription medicines) in 2024 was estimated at around USD 1.5 trillion (EUR 1.41 trillion) at ex-factory prices, which is 9.7% higher than the previous year, according to data from the publication “The Pharmaceutical Industry in Figures” by the European Federation of Pharmaceutical Industries and Associations (EFPIA).

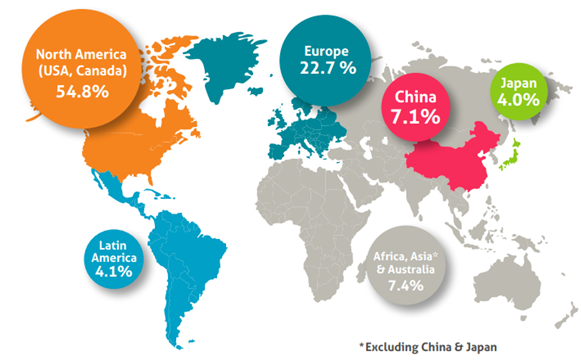

At the end of 2024, the North American region (the USA and Canada) is the world’s largest market with a 54.8% share, far ahead of Europe, China and Japan (Fig. 1). The European region, which in this interpretation includes Turkey, Ukraine, Belarus and the Russian Federation, is in 2nd place with a 22.7% market share, and China is in 3rd place — 7.1%.

Fig. 1. Regional structure of the global prescription pharmaceutical market in 2024, % of the volume in USD

In 2019–2024, the average annual growth rate of the US market was 9.8%; the five largest European markets (Germany, France, Italy, Spain, the United Kingdom) — 7.9%; the Brazilian, Chinese and Indian markets showed growth of 14.3, 2.2 and 9.5% respectively.

According to the latest analysts’ estimates, the global pharmaceutical market (prescription and over-the-counter medicines) in 2024 was about USD 1.6–1.8 billion, and the compound annual growth rates (CAGR) for 2025–2029 are forecast at 5–8%.

Growth is driven by population ageing, rising prevalence of chronic diseases, innovation in biotechnologies and specialised types of therapy.

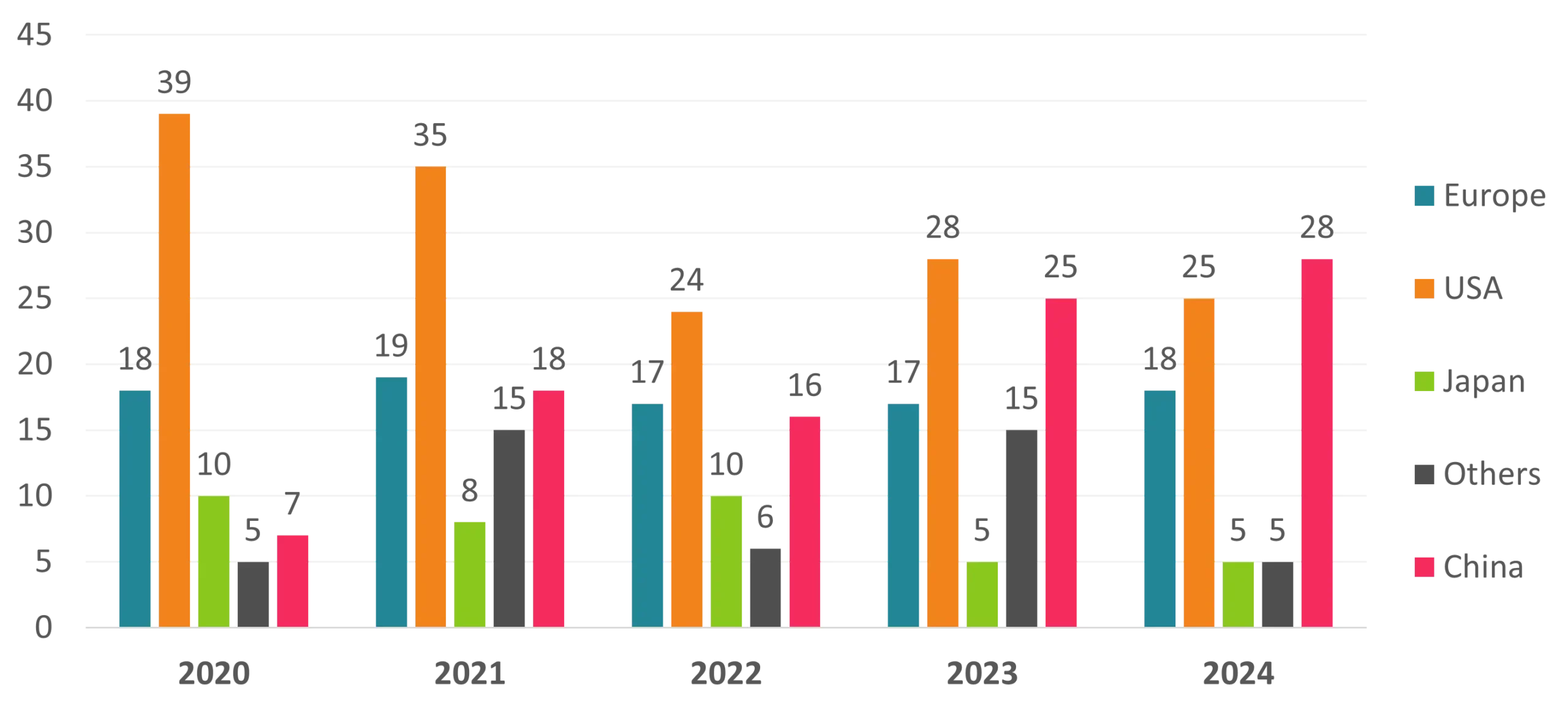

Over the past 5 years, more than 400 new medicines and biologics have been launched worldwide (Fig. 2), more than half of which were developed in the USA (151) and Europe (89). We will look at these largest segments of the pharma market in more detail in the following sections.

Fig. 2. Number of new medicines by region in 2020–2024

By the MAT (Moving annual total) indicator for the period from July 2024 to June 2025, retail sales of “pharmacy basket” products also show confident growth in monetary terms (+20% to UAH 214.3 billion), and almost no movement in natural terms (+1% to 1301.2 million packs).

The USA plays a key and multifaceted role in the global pharmaceutical market — in sales volumes, innovation, investment and regulation. The United States is the largest sales market and the main driver of R&D in the world.

The United States holds the largest share of the global pharmaceutical market, which consistently exceeds 40% of the total volume.

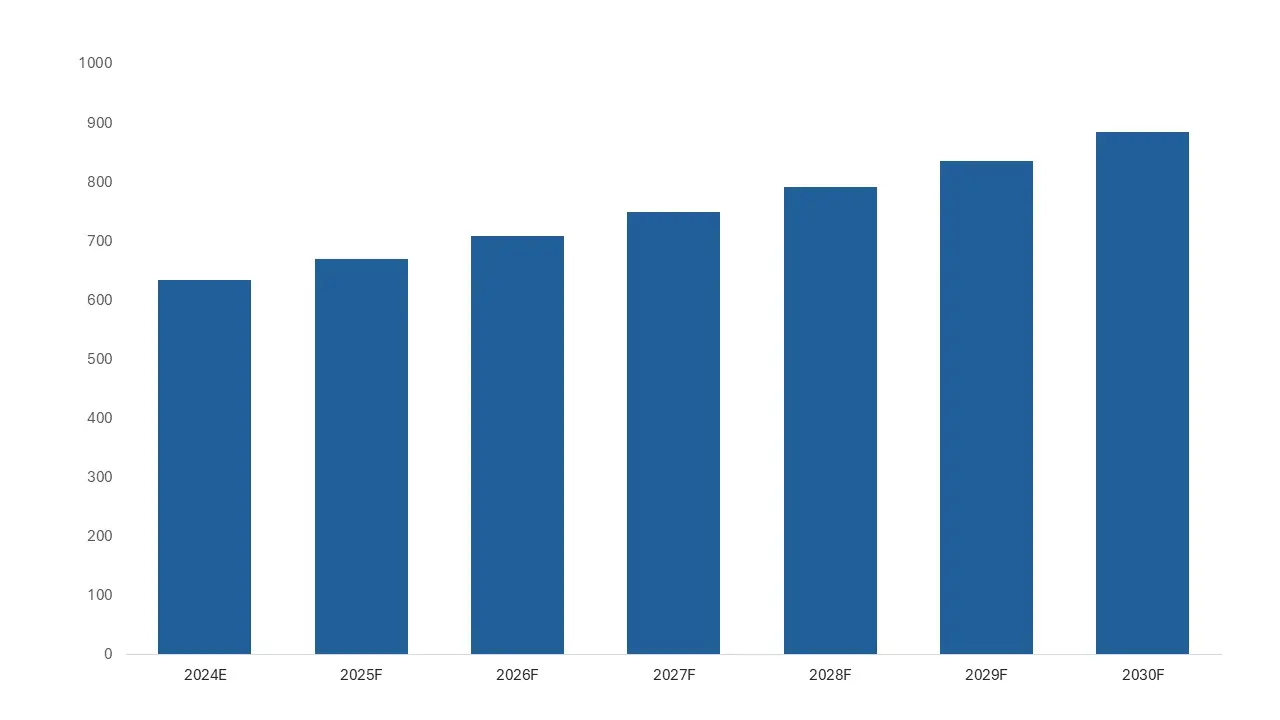

According to industry estimates, the US pharmaceutical market in 2024 was about USD 613–634 billion in revenue, accounting for more than 40% of the global medicines market. It is forecast that by 2030 the market will grow to about USD 857–884 billion at a CAGR of about 5.7% (Fig. 3).

Fig. 3. Estimated size of the US medicines market in 2024 and forecast for 2025–2030, USD billions

The high growth rates of the US pharma market are driven by population ageing and the increasing number of chronic diseases, as well as the population’s access to innovative, specialised and therefore more expensive medicines and therapies.

It is worth noting that the structure of medicines in the USA has a large share of branded and innovative products, whereas in many other countries generics have a larger share. We will consider the US contribution to the creation of new medicines below.

The United States is the world leader in R&D investment. Every year, tens of billions of dollars are invested in the development of new medicines, the search for promising molecules, the creation of new dosage forms and improvement of existing ones, as well as in genetic engineering, cell therapy and the development of biosimilars.

Pharma companies are actively adopting technologies: AI and big data are used to speed up R&D, optimise clinical studies and analyse data.

The United States hosts the largest pharmaceutical and biotechnology companies: Pfizer, J&J, Merck, AbbVie, Bristol-Myers Squibb, Amgen and others, as well as biotechnology “Silicon Valley” hubs — Boston-Cambridge, the San Francisco Bay Area, San Diego. Venture financing of biotech start-ups plays a huge role.

The USA leads in the number of clinical trials and the development of new medicines, including gene and cell therapy.

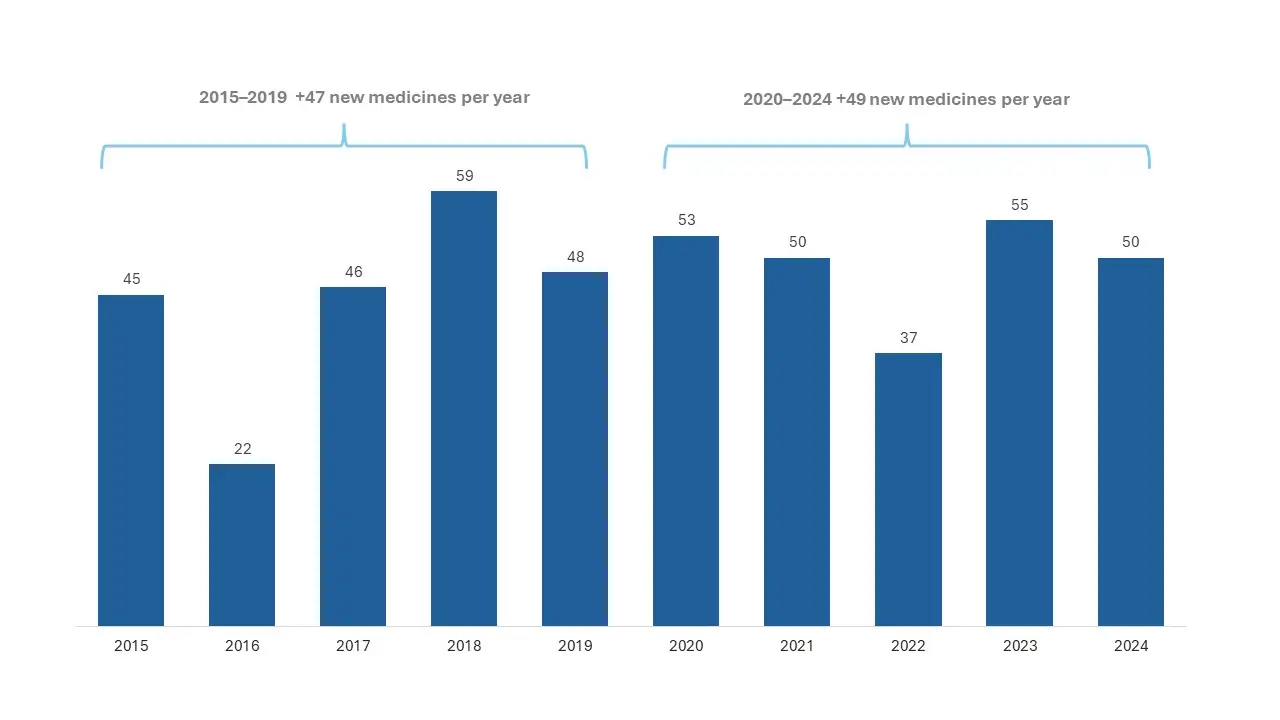

In 2025–2029, more than 250 new innovative medicines are expected to be launched in the USA, based on the 2015–2024 dynamics presented in the “2024 New Drug Therapy Approvals Annual Report” by the Center for Drug Evaluation and Research (CDER) of the US Food and Drug Administration (FDA) (Fig. 4).

Fig. 4. Dynamics of the number of new medicines approved by CDER in the USA in 2015–2024

The 10-year chart below shows that from 2015 to 2024, CDER approved on average about 47 new medicines per year, while over the last 5 years the average is 49 medicines.

CDER identified 24 of the 50 new medicines approved in 2024 (48%) as first-in-class drugs. These medicines have a new pharmacological effect on the body or on a specific biological target in a disease.

In 2024, 26 of the 50 new medicines approved by CDER (52%) were indicated for the treatment of rare or “orphan” diseases (diseases affecting fewer than 200,000 people in the USA). For patients with rare diseases, there are often few or no medicines developed to treat their condition.

It is expected that in the next 5 years about 100 new anticancer medicines will be approved worldwide, most of which will be available in the USA. A significant share of new medicines will be weight-loss and diabetes medicines, as well as other groups of innovative cell and gene therapies, which partly overlap with oncology treatments.

High medicine prices are partly due to the cost of introducing innovations for small groups of patients with high needs for them.

As more and more costly treatment methods appear on the market, the topic of pricing of medicines in the USA remains in the spotlight of the media.

One of the main topics of the US market in 2025 was the policy of reducing medicine prices. The US administration reached agreements with major pharma companies (Pfizer, Merck, GSK, Novartis and others) to reduce medicine prices and align prices for Medicaid with levels in other developed countries, and will also launch the TrumpRx platform for direct sales to consumers. These measures are intended to reduce costs for vulnerable population groups, although the economic effect is still being discussed by experts. This policy reflects growing public and political pressure on the pharma business to reduce patient costs and government spending.

Specialised medicines (for example, for oncology, autoimmune diseases, as well as GLP-1 agonists) account for the lion’s share of medicine spending in the USA and continue to dominate the industry.

The development of biologics and gene therapy creates new opportunities, but also raises questions about cost and reimbursement models.

As for biosimilars, the FDA administration plans to simplify and speed up their approval process, which could strengthen competition, reduce prices for biologics and weaken the monopoly of major brands.

The FDA approved the first oral tablet for the treatment of obesity (semaglutide), which opens a new market segment and increases competition with injectable products.

To improve the efficiency of developing new medicines and reduce research costs, pharma companies are actively implementing digital technologies and AI.

Digital solutions and telemedicine improve interaction with patients and help adapt treatment.

The role of the USA is system-forming. It is the largest sales market, the global centre of innovation, the main investor in medicine development and a regulator that sets standards for the whole world. Many global pharma decisions are made with an eye on the US market.

The US market is characterised by high prices and demand for modern therapies, which makes it the most profitable for pharma companies. Because of high margins, the US market ensures the global payback of innovation.

The FDA is considered one of the most authoritative regulators. FDA approval often opens the path to commercial success worldwide. Through accelerated pathways (Fast Track, Breakthrough Therapy and others), the USA stimulates innovation.

Europe is the second most important centre of global pharmaceuticals. Its distinctive feature is a balance of innovation, socially oriented pricing policy and strong export potential. If the USA is the engine of profits and investment, Europe is the engine of quality, standardisation and sustainable development of the industry.

Europe (the EU + the United Kingdom and others) accounts for about 20–25% of the global pharma market by sales. The main volume is still made up of traditional medicines (small molecules), but biologics and biosimilars are gradually increasing their share in the market.

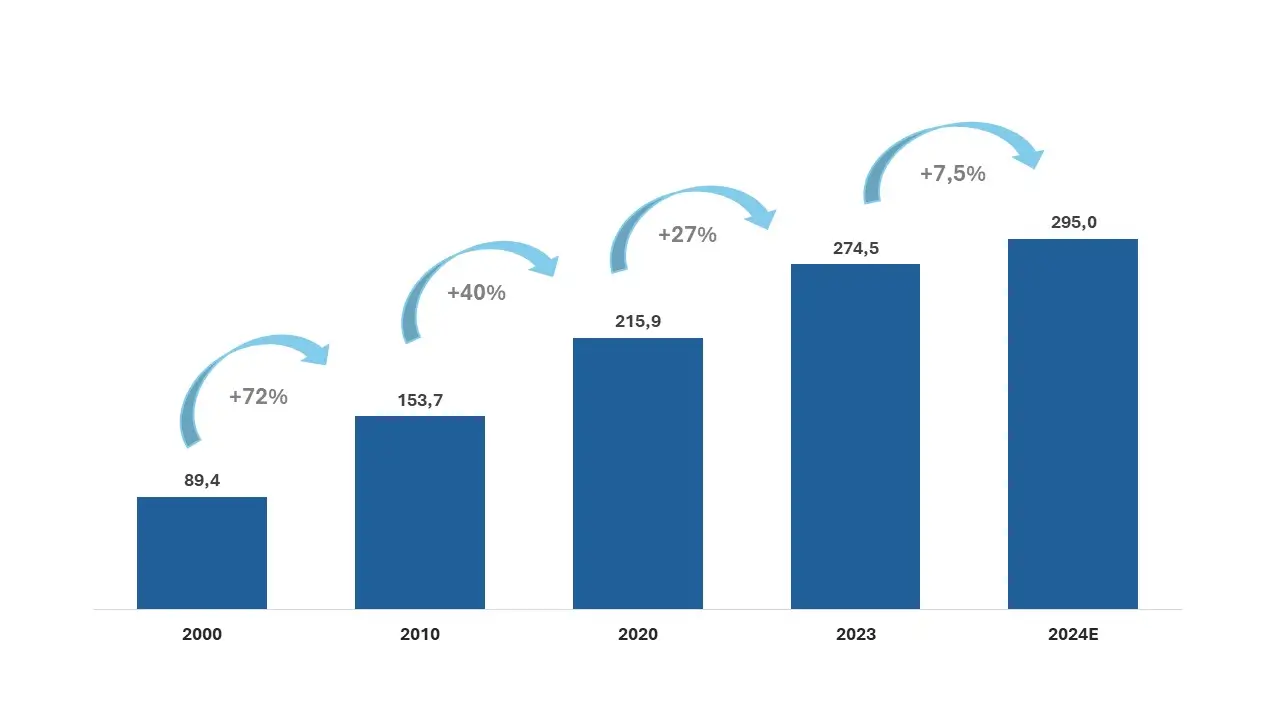

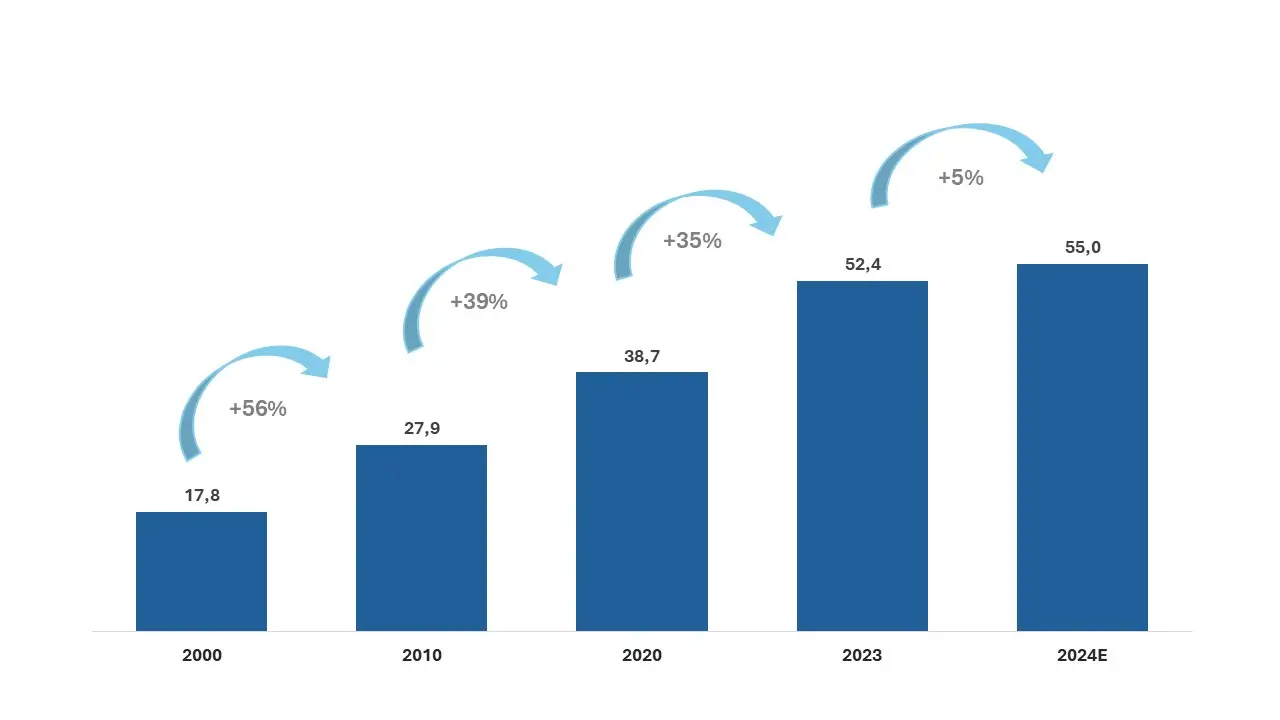

Let us look in more detail at pharma market volumes over time (Fig. 5), as well as its structure, based on the publication “The Pharmaceutical Industry in Figures, Key Data 2025” by the European Federation of Pharmaceutical Industries and Associations (EFPIA).

Fig. 5. Dynamics of the size of the European medicines market with % growth for 2000–2024, EUR billions

The total size of the European pharma market in 2024 is estimated at EUR 295 billion at ex-factory prices, which is 7.5% higher than the previous year. The market dynamics are positive and are expected to continue over the next few years. Factors contributing to market growth include an increase in chronic diseases due to the region’s demographic profile (population ageing), government initiatives to support people’s access to medicines and treatment, large investments in the development of new medicines and therapies, and the growth of digitalisation and online trade in pharma.

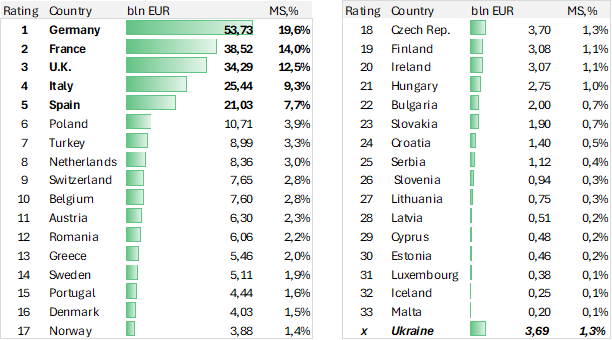

The lion’s share of the European pharma market is held by the five largest national segments: Germany, France, Italy, Spain, the United Kingdom. At the end of 2023, the top-5 share was 63% of total European medicines sales volumes (Fig. 6).

Fig. 6. Ranking of European pharma markets showing share (%) of the total volume in 2023, EUR billions

The Ukrainian pharma market, which has significant potential for growth and development, is intensively moving towards European integration.

Europe is one of the global leaders in pharma R&D. European universities and hospital networks play a huge role in clinical research and basic science. A significant contribution to the industry’s development is made by powerful biotech clusters: Switzerland, the United Kingdom (Oxford–Cambridge–London), Germany, Belgium, the Netherlands, Scandinavia.

Large European pharma companies such as Roche, Novartis, Sanofi, GSK, AstraZeneca, Bayer, and Boehringer Ingelheim produce high-tech medicines and active substances that have proven themselves in:

During 2023–2024, according to EFPIA, more than EUR 100 billion was invested in R&D (Fig. 7).

Fig. 7.Dynamics of R&D investment volume in European pharma with the % increase for 2000–2024, EUR billion

It is expected that over the next five years, one third of new medicines coming to market will be anti-cancer drugs and key clusters in neurology, including rare diseases. Other clusters of innovative medicines include next-generation biotherapeutics, which include cell and gene therapy as well as RNA therapy.

The research-based pharmaceutical industry can play a decisive role in restoring Europe’s economic growth and ensuring its competitiveness in the context of a developing global economy.

Personalised medicine is developing actively, including genetically oriented and targeted therapies. European companies are investing in technologies that make it possible to develop medicines for specific genetic profiles of patients, especially in oncology. This trend expands treatment options and reduces side effects, but it requires complex infrastructure and significant investment.

Biologics (biological medicinal products) remain one of the main driving forces: the market for biological medicines is expanding due to new targeted therapies (oncology, autoimmune diseases). The expiry of patent protection for a number of biologics is stimulating the launch of biosimilars—more affordable and less costly versions of originator products. The European Medicines Agency (EMA) is actively simplifying and optimising pathways for the approval of biosimilars, which increases competition and improves patients’ access to effective therapy.

Digital technologies and AI are becoming an integral part of R&D, manufacturing and clinical trials in Europe. AI helps to accelerate drug design, optimise clinical trials and analyse data.

Digital platforms, telemedicine and digital integration across the care pathway increase access to healthcare and support the management of chronic diseases.

The European Union has recently proposed the Critical Medicines Act—an initiative to reduce dependence on Asian countries for the supply of active pharmaceutical ingredients (APIs), especially antibiotics and other critical medicines. The aim is to strengthen supply-chain resilience, stimulate domestic production and reduce supply risks.

The European Commission aims both to address structural risks and to build pharmaceutical partnerships. It actively encourages the deployment and renovation of reliable manufacturing bases that can ensure localised production of raw materials in Europe.

Ukraine’s pharmaceutical industry is one of the most powerful in Eastern Europe. There are more than 100 licensed industrial manufacturers of medicines operating in Ukraine, and the total medicines market in 2024 amounted to almost USD 4.3 billion. Manufacturers have established the full production cycle for 37 critical medicines based on APIs that are also produced in Ukraine.

Ukraine is gradually joining the response to shortages of critical medicines in the EU: the Ministry of Health and six Ukrainian manufacturers joined the Critical Medicines Alliance (CMA), initiated by the European Commission in early 2024 to address the shortage. The country also participates in healthcare programmes (Horizon Europe, etc.), which enables Ukrainian pharma to contribute to innovation.

Switzerland, Belgium, Ireland and Germany are global hubs for exporting finished medicines. At the same time, part of basic raw-material production has been moved to India and China, creating dependence on supply chains—an issue that is now being actively discussed.

Europe’s pharma business combines the traditional reliability of a socially oriented healthcare system with a growing technological transformation: biotechnology, AI, personalisation, resilience, and local initiatives to strengthen supply chains. At the same time, regulatory constraints, pricing models and global competition create challenges for attracting investment and for long-term industrial sustainability.

Europe plays one of the central roles in the global pharmaceutical market—as a major sales market and as a powerful centre of research, manufacturing and regulation. Unlike the United States, Europe relies on stricter price regulation and a high share of exports, while remaining among the leaders in innovation and production.

Europe sets international standards in pharma and clinical research. The EU has the EMA, one of the world’s most authoritative regulators. European manufacturing quality standards—Good Manufacturing Practice (GMP)—have effectively become a global benchmark.

In Europe, prices and reimbursement conditions for medicines are regulated more strongly than in the United States, which on the one hand restrains prices, but on the other can sometimes slow patients’ access to innovations compared with the United States.

Europe is a leading global exporter of medicines (especially Germany, Switzerland, Ireland, Belgium).

Proxima Research is an international provider of data, technologies and services for healthcare. For more than 30 years, the company has been developing analytical solutions for the pharmaceutical business and helping decision-making based on up-to-date market information.

To receive detailed information about our popular products—Market Audit, Promo Test and Rx Test—please use the feedback form.

Read the continuation of the study: Global pharmaceutical market — analysis of Ukraine and Central Asia

If the topic of the article caught your interest — leave a request. We’ll discuss how this can work for you.

By clicking the “Submit Application” button, you consent to the processing of personal data and to receiving electronic messages about Proxima Research products and services, and you agree to our Terms of Use. Your data will be processed in accordance with our Privacy Policy. You may unsubscribe at any time.

By clicking the “Subscribe” button, you consent to the processing of personal data and the receipt of electronic messages about Proxima Research products and services, and you agree to our Terms of Use. Your data will be processed in accordance with our Privacy Policy. You can unsubscribe at any time.

or